What will an updated overtime rule mean for millions of workers?

Tomorrow, the Vice President is expected to announce the U.S. Department of Labor’s issuance of the final rule on overtime for salaried employees. Rumor has it that the rule will guarantee overtime pay to anyone working more than 40 hours in a week if their salary is less than $47,500 a year or $913 a week. That is less than DOL proposed last year, but still a very significant increase that will mean millions of employees will get raises or have their weekly hours scaled back to a more humane level. About 12.5 million employees will either be newly entitled to overtime pay or will have their rights strengthened so that they don’t have to rely on a complicated analysis of their job duties to determine that they have a right to time and a half for their overtime hours.

Reporters and Hill staffers wonder who are the people who will get raises, a question that is both easy to answer and difficult. The easy part is that employees earning close to, but less than, the new threshold will get raises if they typically work overtime. It will be cheaper and easier for the employer just to give them a raise of a couple of thousand dollars than to track their hours and pay them time and a half.

An obvious example is postdoctoral researchers, who typically earn $42,000 to $45,000, who work 50 to 60 hours a week, or more, conducting critical cancer and other biomedical research, physics, chemistry, biology, or math research. Paying them overtime for their normal, excessive workweek would be so expensive that their universities will give them a raise above the threshold in order to avoid it. The result will not just be better-rewarded researchers, but less turnover and stronger commitments to work that might benefit the entire nation and even the world.

In the comments it submitted for the rule-making record, the American Bankers Association provided good examples of employees in its industry who will benefit. The Bankers testified that banks commonly have various managers, including check processing managers, branch managers, IT managers, credit analysts, and compliance officers, who are currently treated as exempt and are denied overtime pay. But in many areas, their median salaries are fairly low: $45,400 for branch managers in Akron, Ohio and $46,300 in El Paso, Texas. Check Processing Managers in Little Rock, Arkansas earn a median salary of $45,800 while they earn a median $45,200 in Brownsville, Texas. It’s likely that their employers will give them all raises if they currently work even four or five hours of overtime a week.

It gets more difficult to predict when the salaries are lower. Will a university that pays its postdocs an exploitative $38,000 a year give them a raise above the new threshold? It probably depends on whether the postdocs are working more than 50 hours a week, at which point it’s cheaper to pay the threshold salary for exemption than to pay for each hour of overtime at 1.5 times the regular rate of pay.

Many reporters have told me that they are paid less than the salary threshold but are treated as exempt and denied any overtime pay. Reporters in high-cost areas such as New York, Washington, DC, or Boston are almost certainly going to receive salary increases, unless their pay is atypically low. I imagine that even in the South, many reporters are paid enough (and their hours are long enough) that a salary increase will be cheaper for their employer than paying overtime.

They probably won’t all get salary increases, but 2.6 million salaried employees covered by the Fair Labor Standards Act earn between $23,660 and $47,500. If they work substantial amounts of overtime now, they have a good chance that their salaries will be raised above the new exemption threshold.

Trump’s official tax plan blatantly contradicts his populist rhetoric

It’s pretty clear that pinning Donald Trump down on actual policy specifics is going to be tough. He has released a tax plan (written down on actual paper), and until he decides to tear it up, it’s the best road map we have for what he wants to do with tax policy.

The road map charts the course to really large tax cuts, with the bulk of them going to very-high-income households: At the plan’s core is a mostly-routine Republican tax plan that includes giveaways similar to those intended by Marco Rubio, Jeb Bush, and Ted Cruz. The difference is that the plan throws people off the scent of who it benefits, because it contains some novel (and particularly stupid) detours that make no sense as good policy.

When Trump says things like “But the middle class has to be protected. The rich is probably going to end up paying more,” one might come away with the idea that this is a middle-class focused tax cut. The guts of Trump’s tax proposal, however, reveal how obvious of a giveaway to the already-rich it is. To get an idea of just how much money is being doled out, the Tax Policy Center (TPC) estimates that Trump’s plan would cost about $9.5 trillion over a decade. 35 percent of Trump’s tax cuts go to the top 1 percent of households during the first year of his tax plan (TPC estimates that as households making over $732,323 annually). This is more than the combined share that the 80 percent of us making under $142,601 a year can expect to see. And this regressivity actually grows over time: By 2025, the top 1 percent will take about a 40 percent share of the tax cut – almost equivalent to the combined share that the bottom 90 percent will see. The tax cut’s regressivity is highlighted even further by looking at the share within the top 1 percent. About half of the share going to the top 1 percent is actually going to just the top 0.1 percent – households making over $3,769,396 in the first year.

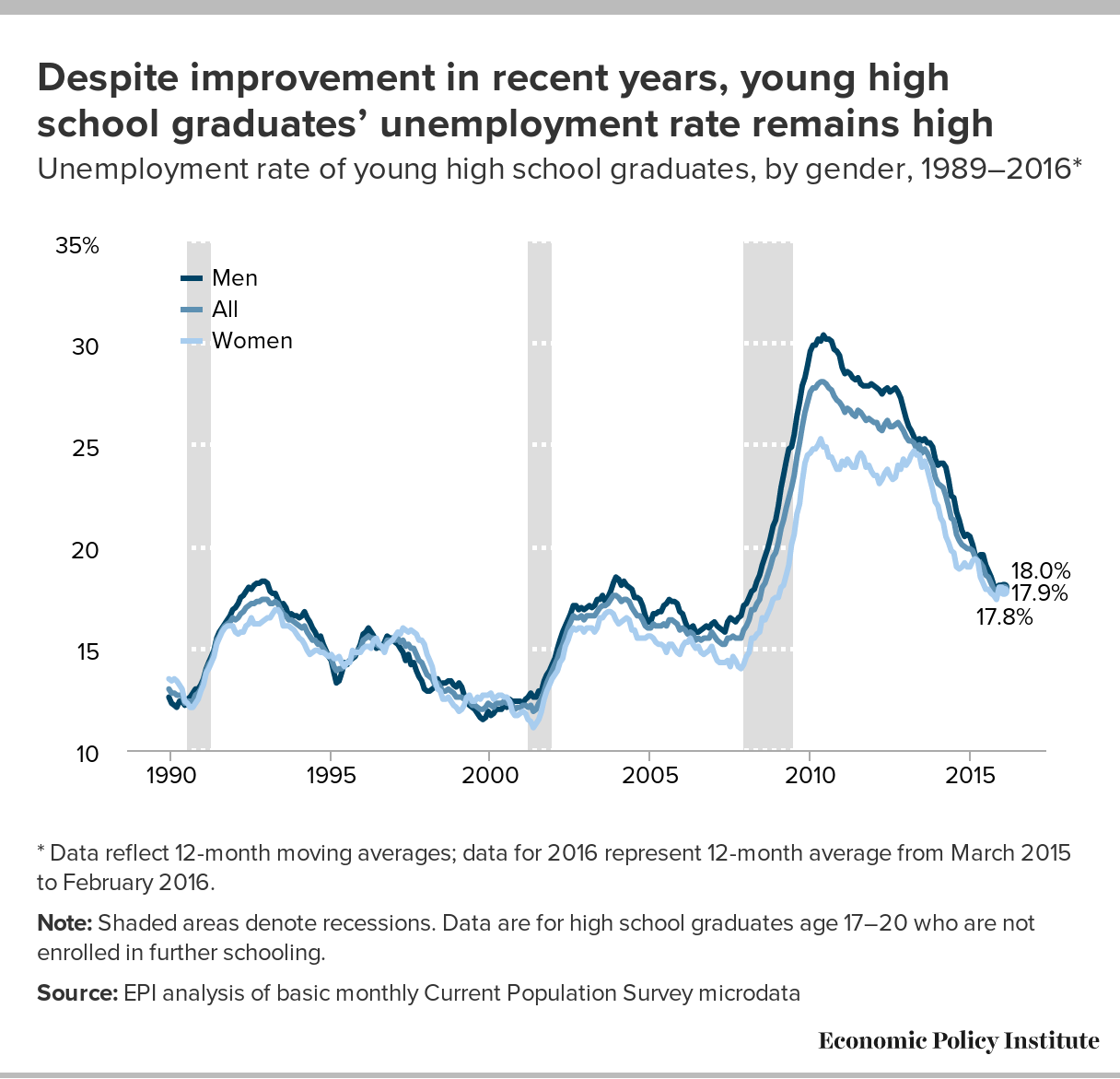

Explaining to Kevin Drum why we’re not happy about young high school grads’ recovery, and why he shouldn’t be either

Mother Jones’ Kevin Drum seems to dislike a New York Times article calling job prospects for young high school graduates “grim.” Along the way, he directs an odd bit of unprovoked snark at us:

I don’t know how EPI measures unemployment, but the federal government measures it in a consistent way every single month. For young high school grads, the average unemployment rate during the expansion of the aughts was around 11 percent. Today it’s 11.2 percent. In other words, it’s not “pretty poor,” it’s completely normal.

Well, we measure unemployment the same way that the federal government does, even using the same survey. All numbers and methods are described in our Class of 2016 paper from a few weeks ago. The reason we get 17.8 percent while Kevin gets 11.2 percent when looking at unemployment rates for young high school graduates is pretty obvious: we’re looking at 17-20 year old high school graduates who are not enrolled in further schooling while he is looking at 20-24 year old high-school graduates (no college). The numbers in our report also reflect a 12-month rolling average, because we also look at smaller demographic groups where sample size is an issue and want consistency across figures.

{kind=link}

A bonus to our data is that we go back to 1989. What this shows is that the 2006 pre-recession trough that we have almost returned to is a pretty low bar for declaring “nothing to see here” on young peoples’ unemployment rates. For the group of young high school grads we look at, the pre-recession unemployment trough was 15.2 percent, but unemployment actually managed to reach 12.3 and 12.0 percent in the unemployment troughs before recessions in the early 1990s and early 2000s. So, yeah, we’re not in love with the 17.9 percent rate we hit in February this year, and we don’t think we’re “wildly misstating” the data to make the case that others shouldn’t be either.

Hires need to pick up to eat away at the weak employment-to-population ratio

On the heels of last week’s latest disappointing jobs numbers, today’s Job Openings and Labor Turnover Survey (JOLTS) report, unsurprisingly, shows little improvement in the labor market. In March, overall job openings rose slightly, while the number of people hired decreased. When we look at these numbers over the year, there has been a marked improvement in job openings—an increase in the rate of job openings (the number of job openings as a share of total employment plus job openings) from 3.5 to 3.9. Over that same period, the hires rate only increased from 3.6 to 3.7—a far slower improvement.

In today’s economy—as opposed to decades past—the listing of job openings is relatively easy and inexpensive, and may not accurately reflect an employer’s efforts to actually fill those openings. Employers may be interested in filling those positions at lower wages than would be required in a stronger labor market. They may not be searching intensively to find workers or willing to fill those positions if they have to offer higher wages. Considering the number of unemployed workers in the economy and the number of missing workers waiting on the sidelines for more opportunities, it seems that many of these openings could be filled if employers were more serious about filing them. It’s fairly straightforward economics at play here. If employers are unhappy with the pool of applicants, they simply might need to improve the job offering—the wages and benefits being offered—to recruit the candidates they desire. When that happens, we should see better wage growth than we’ve seen in the last several years of the recovery.

Housing segregation undergirds the nation’s racial inequities

In June, the Supreme Court rescued the Fair Housing Act from a claim that it prohibited only overt discrimination—where a government body announces that it is enacting a housing policy for racially discriminatory reasons. Instead, Justice Anthony Kennedy’s opinion concluded that housing policies that have the effect of reinforcing segregation must be avoided, regardless of policymakers’ provable intent, unless an agency enacting such a policy can show that there was no reasonable alternative to segregation as a way to accomplish legitimate housing objectives.1

These days, when few public officials are so incautious as to announce they are racists, a different Court decision would have hamstrung efforts to desegregate housing nationwide.

Justice Kennedy based his ruling, in part, on a brief submitted by “Housing Scholars” organized by the Haas Institute and the Economic Policy Institute.2 The brief recounted the long history of government sponsorship of racial segregation that had established the nation’s racial housing patterns. The Housing Scholars argued that, because of entrenched patterns attributable to government policy, seemingly race-neutral policies could have the effect of reinforcing the segregation that government had helped put in place.

Now, a federal appeals court based in California, again relying in part on the Housing Scholars brief, has developed Justice Kennedy’s theory further. The case arose from the refusal of the City of Yuma, Arizona to permit construction of moderate-cost single family homes adjacent to a neighborhood where homes were more expensive.3 Although opponents of the development never said openly that their objection was based on race, they attacked the proposal using code words alleging that the development would bring crime into the neighborhood, that some of the homes might be purchased by single-parent families, and that “unattended children would roam the streets.” (The appeals court observed that where whites are involved, it is called “letting children play in the neighborhood.”) The court said that a reasonable jury could interpret such objections as racially motivated.

A disappointing jobs report overall

This morning’s employment situation report from the Bureau of Labor Statistics showed that the economy added 160,000 jobs in April and the unemployment rate held steady at 5.0 percent, while the labor force participation rate (LFPR) and the employment-to-population ratio (EPOP) ticked down. Nominal hourly wage growth held its recent trend, coming in at 2.5 percent over the year.

Payroll employment growth of 160,000 is notably slower than recent months. Even with the downward revisions to March, job growth looks slower than first quarter of this year (averaging 203,000) or last quarter of 2015 (averaging 282,000). While it is true that as the economy reaches full employment, job growth would be expected to slow, we are not nearly close enough to full employment to view this slow down as a positive move. Given that the first quarter GDP numbers came in so weak as well (0.5 percent annualized), it’s unlikely April’s low growth is a data blip that will be significantly revised upwards.

April payroll employment growth disappoints

| Date | Average monthly growth in non-farm payroll |

|---|---|

| Q4 2015 | 282 |

| Q1 2016 | 203 |

| April 2016 | 160 |

Source: Bureau of Labor Statistics Current Employment Statistics public data series

The White House attacks the spread of abusive non-compete agreements

The White House released a report this morning that illuminates another part of the complex problem of stagnating wages—the rise of non-compete agreements and their spread to low-wage employment. Non-compete agreements, or “non-competes,” are contracts that ban workers at one company from going to work for a competing employer within a certain period of time after leaving a job. They can make sense when a worker has trade secrets or intellectual property in which the employer has invested. But they make no sense when applied to health care workers, retail and restaurant employees, and other low wage employees. All they do is limit opportunity and shackle people to an employer who will have less incentive to give a raise to retain them.

Employers are imposing non-competes in occupations with no possible trade secret justification—even doggy day care providers! The Treasury Department has found that one in seven Americans earning less than $40,000 a year is subject to a non-compete. This is astonishing, and shows how easily businesses abuse their power over employees and restrict their rights, as they increasingly do with forced arbitration clauses that take away the right of workers to seek justice in the courts. In both cases, workers often accept jobs without ever knowing that they have signed their rights away.

The Treasury Department has done groundbreaking work to show that non-competes have a measurable, negative effect on wages, as one would expect from a practice that limits employee mobility. The report also provides evidence that non-competes can reduce entrepreneurship and innovation.

U.S.-Korea trade deal resulted in growing trade deficits and more than 95,000 lost U.S. jobs

(This blog post is an update to a post from March 30, 2015).

When the U.S.-Korea Free Trade Agreement (KORUS) was passed just over four years ago, President Obama said that the agreement would support 70,000 U.S. jobs. This claim was supported by a White House fact sheet that claimed that the KORUS agreement would “increase exports of American goods by $10 to $11 billion…” and that they would “support 70,000 American jobs from increased goods exports alone.” Things are not turning out as predicted. Far from supporting jobs, growing goods trade deficits with Korea have eliminated more than 95,000 jobs between 2011 and 2015.

Expanding exports alone is not enough to ensure that trade adds jobs to the economy. Increases in U.S. exports tend to create jobs in the United States, but increases in imports lead to job loss—by destroying existing jobs and preventing new job creation—as imports displace goods that otherwise would have been made in the United States by domestic workers. Thus, it is changes in trade balances—the net of exports and imports—that determine the number of jobs created or displaced by trade and investment deals like KORUS.

In the first four years after KORUS took effect, there was absolutely no growth in total U.S. exports to Korea, as shown in the figure below. Imports from Korea increased $15.2 billion, an increase of 26.8 percent. As a result, the U.S. trade deficit with Korea increased $15.1 billion between 2011 and 2015, an increase of 114.6 percent, more than doubling in just four years.

U.S.-Korea trade, 2011–2015 (billions of dollars)

| Exports | Imports | Trade balance | |

|---|---|---|---|

| 2011 | $43.5 | 56.7 | -13.2 |

| 2012 | 42.3 | 58.9 | -16.6 |

| 2013 | 41.7 | 62.4 | -20.7 |

| 2014 | 44.5 | 69.5 | -25.0 |

| 2015 | 43.5 | 71.8 | -28.3 |

Change, billions of dollars, and percent from 2011-2015

Imports: +$15.2 (26.8%)

Exports: $0 (0.0%)

Trade Bal.: -$15.1 (114.6%)

Source: Author's analysis of U.S. International Trade Commission Trade DataWeb

What to watch on Jobs Day: Wages, wages, and more wages

Last week, the Federal Open Market Committee rightfully decided against another interest rate increase. Raising rates serves to slow the economy down and, at this point in the recovery, the economy still needs all the help it can get to keep growing. Gross domestic product (GDP) showed a slow rate of growth of 0.5 percent annualized in the first quarter of 2016, following just 1.4 percent growth in the last quarter of 2015. As my colleague Josh Bivens wrote, “if such slow growth continues into 2016, there will be significant upward pressure on unemployment and recent gains in labor force participation will likely fade away.” While we all hope that GDP growth for the first quarter gets revised significantly upwards, and that the last 6 months are more of a blip than a new trend, it is certainly the case that the Fed’s decision to not raise rates looks justified by the data.

Private sector nominal wage growth is one of the top indicators to watch on Friday, and one of the indicators the Fed tracks most closely in making their decisions. Last week, however, we got another useful measure of labor compensation growth. The Bureau of Labor Statistics (BLS) released its latest compensation data from the Employment Cost Index (ECI) for March 2016. The data on wages and salaries from the ECI very much confirm the monthly nominal wage growth numbers that appear every month in the Employment Report (with data from the Current Employment Statistics (CES)). Over the year, private industry wages and salaries as measured by the ECI increased 2.0 percent, while overall compensation costs increased 1.8 percent. Turning to the monthly CES data, wages grew 2.3 percent for the year ending in March 2016.

ANCOR vastly overstates the impact of the overtime rule on community service providers

The Department of Labor (DOL) is about to release a final rule that will require overtime pay for millions of salaried employees who currently can be required to work long hours for no more pay than they receive for a 40-hour week. This will give them either more money or more time with their families or for themselves.

But the overtime rule naturally makes some employers unhappy, since they can currently get 60 hours of work from many employees for only 40 hours of pay. Even some non-profit human service providers, many of which are not even covered by the Fair Labor Standards Act (FLSA), oppose DOL’s updated rule.

An association of community providers serving people with intellectual and developmental disabilities (the American Network of Community Options and Resources, or ANCOR) commissioned a “Cost Impact Scoring Memo” by a company called Avalere to estimate the impact of the proposed overtime rule on its member agencies. Neither the survey questions, the actual responses, nor the response rate were included in Avalere’s report. But it is clear that the cost estimates are deeply flawed.

College degrees are not the solution to stagnating wages or inequality

Our recent report on the class of 2016 showed that young high school and college graduates still face high levels of unemployment and stagnant wages, even though the labor market has improved since the Great Recession. Between these two groups, however, young high school graduates face a far less forgiving economic reality: the unemployment rate for young high school graduates is over three times higher than their college-educated peers (17.9 percent versus 5.6 percent), nearly one in seven is stuck in a part-time job when they really want full-time work, and the wages of entry-level jobs have barely budged since 2000.

Despite improvement in recent years, young high school graduates' unemployment rate remains high: Unemployment rate of young high school graduates, by gender, 1989–2016*

| Date | All | Men | Women |

|---|---|---|---|

| 1989-12-01 | 13.0% | 12.6% | 13.5% |

| 1990-01-01 | 12.8% | 12.3% | 13.4% |

| 1990-02-01 | 12.8% | 12.2% | 13.5% |

| 1990-03-01 | 12.7% | 12.1% | 13.4% |

| 1990-04-01 | 12.7% | 12.4% | 13.2% |

| 1990-05-01 | 12.7% | 12.4% | 13.0% |

| 1990-06-01 | 12.3% | 12.2% | 12.4% |

| 1990-07-01 | 12.4% | 12.5% | 12.3% |

| 1990-08-01 | 12.4% | 12.6% | 12.1% |

| 1990-09-01 | 12.4% | 12.8% | 12.1% |

| 1990-10-01 | 12.7% | 13.0% | 12.3% |

| 1990-11-01 | 12.8% | 13.0% | 12.5% |

| 1990-12-01 | 13.0% | 13.2% | 12.9% |

| 1991-01-01 | 13.4% | 13.5% | 13.2% |

| 1991-02-01 | 13.9% | 14.0% | 13.8% |

| 1991-03-01 | 14.2% | 14.3% | 14.0% |

| 1991-04-01 | 14.4% | 14.6% | 14.3% |

| 1991-05-01 | 14.8% | 14.9% | 14.6% |

| 1991-06-01 | 15.4% | 15.5% | 15.2% |

| 1991-07-01 | 15.6% | 15.8% | 15.5% |

| 1991-08-01 | 15.9% | 16.0% | 15.8% |

| 1991-09-01 | 16.1% | 16.2% | 16.0% |

| 1991-10-01 | 16.2% | 16.4% | 16.1% |

| 1991-11-01 | 16.3% | 16.6% | 16.1% |

| 1991-12-01 | 16.5% | 16.9% | 16.1% |

| 1992-01-01 | 16.4% | 17.0% | 15.8% |

| 1992-02-01 | 16.5% | 17.2% | 15.7% |

| 1992-03-01 | 16.7% | 17.5% | 15.8% |

| 1992-04-01 | 16.8% | 17.6% | 15.8% |

| 1992-05-01 | 17.0% | 17.8% | 16.1% |

| 1992-06-01 | 17.1% | 18.0% | 16.2% |

| 1992-07-01 | 17.2% | 17.9% | 16.5% |

| 1992-08-01 | 17.2% | 18.1% | 16.2% |

| 1992-09-01 | 17.3% | 18.2% | 16.2% |

| 1992-10-01 | 17.3% | 18.2% | 16.2% |

| 1992-11-01 | 17.4% | 18.3% | 16.3% |

| 1992-12-01 | 17.4% | 18.3% | 16.4% |

| 1993-01-01 | 17.4% | 18.2% | 16.5% |

| 1993-02-01 | 17.2% | 17.8% | 16.5% |

| 1993-03-01 | 17.2% | 17.7% | 16.7% |

| 1993-04-01 | 17.3% | 17.7% | 16.9% |

| 1993-05-01 | 17.2% | 17.4% | 16.9% |

| 1993-06-01 | 16.9% | 17.1% | 16.7% |

| 1993-07-01 | 16.7% | 17.2% | 16.1% |

| 1993-08-01 | 16.6% | 17.0% | 16.1% |

| 1993-09-01 | 16.4% | 16.6% | 16.1% |

| 1993-10-01 | 16.4% | 16.7% | 16.0% |

| 1993-11-01 | 16.3% | 16.6% | 15.9% |

| 1993-12-01 | 16.2% | 16.6% | 15.7% |

| 1994-01-01 | 16.1% | 16.5% | 15.5% |

| 1994-02-01 | 16.0% | 16.6% | 15.4% |

| 1994-03-01 | 16.1% | 16.8% | 15.2% |

| 1994-04-01 | 15.8% | 16.5% | 14.9% |

| 1994-05-01 | 15.6% | 16.3% | 14.7% |

| 1994-06-01 | 15.4% | 16.0% | 14.8% |

| 1994-07-01 | 15.4% | 15.8% | 14.9% |

| 1994-08-01 | 15.2% | 15.5% | 14.9% |

| 1994-09-01 | 15.2% | 15.6% | 14.8% |

| 1994-10-01 | 15.0% | 15.2% | 14.8% |

| 1994-11-01 | 14.8% | 14.9% | 14.7% |

| 1994-12-01 | 14.6% | 14.6% | 14.6% |

| 1995-01-01 | 14.5% | 14.4% | 14.7% |

| 1995-02-01 | 14.1% | 13.8% | 14.5% |

| 1995-03-01 | 13.9% | 13.3% | 14.5% |

| 1995-04-01 | 14.0% | 13.4% | 14.6% |

| 1995-05-01 | 14.0% | 13.8% | 14.3% |

| 1995-06-01 | 14.2% | 14.3% | 14.1% |

| 1995-07-01 | 14.3% | 14.2% | 14.3% |

| 1995-08-01 | 14.4% | 14.4% | 14.3% |

| 1995-09-01 | 14.6% | 14.5% | 14.9% |

| 1995-10-01 | 14.7% | 14.6% | 14.8% |

| 1995-11-01 | 14.9% | 14.9% | 14.8% |

| 1995-12-01 | 15.0% | 15.2% | 14.8% |

| 1996-01-01 | 15.4% | 15.7% | 15.0% |

| 1996-02-01 | 15.5% | 15.8% | 15.1% |

| 1996-03-01 | 15.6% | 16.0% | 15.1% |

| 1996-04-01 | 15.5% | 15.8% | 15.0% |

| 1996-05-01 | 15.5% | 15.6% | 15.4% |

| 1996-06-01 | 15.2% | 15.0% | 15.5% |

| 1996-07-01 | 15.1% | 15.1% | 15.2% |

| 1996-08-01 | 15.1% | 15.0% | 15.1% |

| 1996-09-01 | 15.1% | 15.3% | 14.8% |

| 1996-10-01 | 15.4% | 15.6% | 15.2% |

| 1996-11-01 | 15.4% | 15.5% | 15.3% |

| 1996-12-01 | 15.4% | 15.5% | 15.4% |

| 1997-01-01 | 15.4% | 15.3% | 15.6% |

| 1997-02-01 | 15.5% | 15.2% | 15.8% |

| 1997-03-01 | 15.3% | 15.0% | 15.7% |

| 1997-04-01 | 15.4% | 14.8% | 16.0% |

| 1997-05-01 | 15.1% | 14.4% | 15.9% |

| 1997-06-01 | 15.2% | 14.7% | 15.8% |

| 1997-07-01 | 15.0% | 14.2% | 15.9% |

| 1997-08-01 | 15.0% | 14.3% | 15.8% |

| 1997-09-01 | 14.7% | 13.9% | 15.7% |

| 1997-10-01 | 14.4% | 13.6% | 15.4% |

| 1997-11-01 | 14.3% | 13.4% | 15.4% |

| 1997-12-01 | 14.0% | 13.0% | 15.2% |

| 1998-01-01 | 13.7% | 12.9% | 14.7% |

| 1998-02-01 | 13.6% | 12.9% | 14.4% |

| 1998-03-01 | 13.5% | 13.0% | 14.1% |

| 1998-04-01 | 13.2% | 13.1% | 13.4% |

| 1998-05-01 | 13.3% | 13.5% | 13.0% |

| 1998-06-01 | 13.1% | 13.2% | 12.9% |

| 1998-07-01 | 12.9% | 13.3% | 12.5% |

| 1998-08-01 | 12.9% | 13.3% | 12.5% |

| 1998-09-01 | 13.0% | 13.4% | 12.6% |

| 1998-10-01 | 12.9% | 13.4% | 12.4% |

| 1998-11-01 | 12.8% | 13.2% | 12.2% |

| 1998-12-01 | 12.6% | 13.1% | 12.1% |

| 1999-01-01 | 12.6% | 13.3% | 11.9% |

| 1999-02-01 | 12.6% | 13.1% | 12.0% |

| 1999-03-01 | 12.5% | 12.7% | 12.2% |

| 1999-04-01 | 12.6% | 12.5% | 12.6% |

| 1999-05-01 | 12.4% | 12.2% | 12.7% |

| 1999-06-01 | 12.2% | 12.1% | 12.4% |

| 1999-07-01 | 12.2% | 12.0% | 12.4% |

| 1999-08-01 | 12.1% | 11.8% | 12.6% |

| 1999-09-01 | 12.0% | 11.6% | 12.5% |

| 1999-10-01 | 12.0% | 11.5% | 12.7% |

| 1999-11-01 | 12.1% | 11.6% | 12.7% |

| 1999-12-01 | 12.3% | 11.9% | 12.7% |

| 2000-01-01 | 12.2% | 11.7% | 12.8% |

| 2000-02-01 | 12.1% | 11.8% | 12.5% |

| 2000-03-01 | 12.3% | 12.0% | 12.6% |

| 2000-04-01 | 12.3% | 12.0% | 12.7% |

| 2000-05-01 | 12.3% | 12.0% | 12.7% |

| 2000-06-01 | 12.4% | 12.2% | 12.6% |

| 2000-07-01 | 12.3% | 12.1% | 12.6% |

| 2000-08-01 | 12.4% | 12.5% | 12.4% |

| 2000-09-01 | 12.2% | 12.4% | 11.9% |

| 2000-10-01 | 12.0% | 12.4% | 11.7% |

| 2000-11-01 | 12.1% | 12.4% | 11.7% |

| 2000-12-01 | 12.1% | 12.4% | 11.8% |

| 2001-01-01 | 12.2% | 12.3% | 11.9% |

| 2001-02-01 | 12.2% | 12.5% | 11.8% |

| 2001-03-01 | 12.1% | 12.6% | 11.5% |

| 2001-04-01 | 12.2% | 12.8% | 11.4% |

| 2001-05-01 | 11.9% | 12.6% | 11.1% |

| 2001-06-01 | 12.0% | 12.6% | 11.3% |

| 2001-07-01 | 12.3% | 12.9% | 11.5% |

| 2001-08-01 | 12.5% | 12.9% | 11.9% |

| 2001-09-01 | 12.9% | 13.4% | 12.5% |

| 2001-10-01 | 13.3% | 13.7% | 12.9% |

| 2001-11-01 | 13.6% | 13.9% | 13.2% |

| 2001-12-01 | 13.9% | 14.2% | 13.5% |

| 2002-01-01 | 14.2% | 14.5% | 13.7% |

| 2002-02-01 | 14.5% | 15.0% | 13.9% |

| 2002-03-01 | 14.9% | 15.4% | 14.3% |

| 2002-04-01 | 15.2% | 15.8% | 14.5% |

| 2002-05-01 | 15.6% | 16.1% | 15.1% |

| 2002-06-01 | 16.0% | 16.4% | 15.4% |

| 2002-07-01 | 16.3% | 16.7% | 15.8% |

| 2002-08-01 | 16.6% | 17.1% | 16.0% |

| 2002-09-01 | 16.5% | 17.1% | 15.9% |

| 2002-10-01 | 16.5% | 16.9% | 16.0% |

| 2002-11-01 | 16.6% | 17.0% | 16.0% |

| 2002-12-01 | 16.4% | 16.9% | 15.8% |

| 2003-01-01 | 16.6% | 17.0% | 16.0% |

| 2003-02-01 | 16.6% | 17.1% | 16.0% |

| 2003-03-01 | 16.6% | 17.0% | 16.0% |

| 2003-04-01 | 16.6% | 17.1% | 15.8% |

| 2003-05-01 | 16.8% | 17.4% | 16.0% |

| 2003-06-01 | 17.0% | 17.4% | 16.5% |

| 2003-07-01 | 17.1% | 17.6% | 16.5% |

| 2003-08-01 | 17.1% | 17.3% | 16.7% |

| 2003-09-01 | 17.2% | 17.5% | 16.8% |

| 2003-10-01 | 17.4% | 17.8% | 16.8% |

| 2003-11-01 | 17.6% | 18.2% | 16.7% |

| 2003-12-01 | 17.6% | 18.5% | 16.4% |

| 2004-01-01 | 17.5% | 18.4% | 16.2% |

| 2004-02-01 | 17.3% | 18.1% | 16.3% |

| 2004-03-01 | 17.4% | 18.3% | 16.4% |

| 2004-04-01 | 17.4% | 18.1% | 16.5% |

| 2004-05-01 | 17.3% | 18.0% | 16.4% |

| 2004-06-01 | 17.0% | 17.9% | 15.9% |

| 2004-07-01 | 16.8% | 17.5% | 15.9% |

| 2004-08-01 | 16.6% | 17.5% | 15.5% |

| 2004-09-01 | 16.6% | 17.4% | 15.5% |

| 2004-10-01 | 16.4% | 17.1% | 15.5% |

| 2004-11-01 | 16.1% | 16.6% | 15.5% |

| 2004-12-01 | 16.0% | 16.3% | 15.6% |

| 2005-01-01 | 16.0% | 16.3% | 15.6% |

| 2005-02-01 | 16.2% | 16.7% | 15.5% |

| 2005-03-01 | 16.1% | 16.7% | 15.3% |

| 2005-04-01 | 16.1% | 16.8% | 15.2% |

| 2005-05-01 | 16.1% | 16.8% | 15.2% |

| 2005-06-01 | 16.2% | 17.1% | 15.1% |

| 2005-07-01 | 16.1% | 17.2% | 14.8% |

| 2005-08-01 | 16.4% | 17.4% | 15.2% |

| 2005-09-01 | 16.4% | 17.3% | 15.2% |

| 2005-10-01 | 16.3% | 17.3% | 15.0% |

| 2005-11-01 | 16.2% | 17.2% | 14.8% |

| 2005-12-01 | 15.9% | 16.8% | 14.7% |

| 2006-01-01 | 16.0% | 16.7% | 15.1% |

| 2006-02-01 | 15.9% | 16.3% | 15.3% |

| 2006-03-01 | 15.7% | 16.0% | 15.3% |

| 2006-04-01 | 15.8% | 16.0% | 15.5% |

| 2006-05-01 | 15.7% | 16.1% | 15.2% |

| 2006-06-01 | 15.4% | 15.8% | 15.0% |

| 2006-07-01 | 15.5% | 15.8% | 15.1% |

| 2006-08-01 | 15.4% | 15.9% | 14.8% |

| 2006-09-01 | 15.5% | 16.0% | 14.7% |

| 2006-10-01 | 15.5% | 16.1% | 14.8% |

| 2006-11-01 | 15.5% | 16.0% | 14.9% |

| 2006-12-01 | 15.8% | 16.2% | 15.1% |

| 2007-01-01 | 15.6% | 16.3% | 14.7% |

| 2007-02-01 | 15.4% | 16.1% | 14.4% |

| 2007-03-01 | 15.3% | 16.0% | 14.3% |

| 2007-04-01 | 15.2% | 15.9% | 14.3% |

| 2007-05-01 | 15.2% | 15.8% | 14.3% |

| 2007-06-01 | 15.5% | 16.3% | 14.4% |

| 2007-07-01 | 15.5% | 16.5% | 14.1% |

| 2007-08-01 | 15.6% | 16.4% | 14.6% |

| 2007-09-01 | 15.5% | 16.3% | 14.4% |

| 2007-10-01 | 15.5% | 16.5% | 14.1% |

| 2007-11-01 | 15.5% | 16.6% | 14.0% |

| 2007-12-01 | 15.9% | 17.1% | 14.2% |

| 2008-01-01 | 16.1% | 17.2% | 14.6% |

| 2008-02-01 | 16.4% | 17.5% | 14.8% |

| 2008-03-01 | 16.9% | 17.8% | 15.5% |

| 2008-04-01 | 16.9% | 17.9% | 15.5% |

| 2008-05-01 | 17.2% | 18.3% | 15.7% |

| 2008-06-01 | 17.4% | 18.6% | 15.8% |

| 2008-07-01 | 18.0% | 19.1% | 16.5% |

| 2008-08-01 | 18.2% | 19.5% | 16.4% |

| 2008-09-01 | 18.6% | 19.9% | 16.7% |

| 2008-10-01 | 19.0% | 20.4% | 17.0% |

| 2008-11-01 | 19.5% | 21.0% | 17.4% |

| 2008-12-01 | 19.7% | 21.3% | 17.5% |

| 2009-01-01 | 20.2% | 22.0% | 17.5% |

| 2009-02-01 | 20.9% | 22.9% | 18.0% |

| 2009-03-01 | 21.3% | 23.5% | 18.1% |

| 2009-04-01 | 21.9% | 24.2% | 18.6% |

| 2009-05-01 | 22.4% | 24.8% | 19.1% |

| 2009-06-01 | 22.9% | 24.9% | 20.1% |

| 2009-07-01 | 23.5% | 25.5% | 20.6% |

| 2009-08-01 | 24.4% | 26.4% | 21.6% |

| 2009-09-01 | 25.1% | 27.1% | 22.1% |

| 2009-10-01 | 25.9% | 27.9% | 23.2% |

| 2009-11-01 | 26.6% | 28.3% | 24.1% |

| 2009-12-01 | 27.1% | 28.9% | 24.5% |

| 2010-01-01 | 27.6% | 29.6% | 24.6% |

| 2010-02-01 | 27.8% | 29.9% | 24.8% |

| 2010-03-01 | 27.8% | 29.9% | 24.8% |

| 2010-04-01 | 28.0% | 30.2% | 25.0% |

| 2010-05-01 | 28.1% | 30.1% | 25.3% |

| 2010-06-01 | 28.1% | 30.4% | 24.9% |

| 2010-07-01 | 28.0% | 30.2% | 24.9% |

| 2010-08-01 | 27.8% | 30.2% | 24.4% |

| 2010-09-01 | 27.7% | 30.1% | 24.4% |

| 2010-10-01 | 27.4% | 29.7% | 24.1% |

| 2010-11-01 | 27.2% | 29.6% | 23.8% |

| 2010-12-01 | 27.1% | 29.4% | 23.8% |

| 2011-01-01 | 26.9% | 28.8% | 24.2% |

| 2011-02-01 | 26.6% | 28.5% | 24.0% |

| 2011-03-01 | 26.8% | 28.6% | 24.3% |

| 2011-04-01 | 26.7% | 28.5% | 24.1% |

| 2011-05-01 | 26.5% | 28.3% | 23.9% |

| 2011-06-01 | 26.4% | 28.2% | 23.9% |

| 2011-07-01 | 26.7% | 28.3% | 24.4% |

| 2011-08-01 | 26.6% | 28.0% | 24.6% |

| 2011-09-01 | 26.4% | 27.9% | 24.4% |

| 2011-10-01 | 26.2% | 27.9% | 23.9% |

| 2011-11-01 | 26.3% | 27.9% | 24.0% |

| 2011-12-01 | 26.2% | 28.0% | 23.7% |

| 2012-01-01 | 26.1% | 27.9% | 23.5% |

| 2012-02-01 | 26.1% | 27.8% | 23.5% |

| 2012-03-01 | 25.8% | 27.7% | 23.1% |

| 2012-04-01 | 25.7% | 27.5% | 23.3% |

| 2012-05-01 | 26.0% | 27.7% | 23.6% |

| 2012-06-01 | 26.2% | 27.8% | 23.8% |

| 2012-07-01 | 25.9% | 27.6% | 23.5% |

| 2012-08-01 | 25.9% | 27.7% | 23.3% |

| 2012-09-01 | 26.0% | 27.8% | 23.4% |

| 2012-10-01 | 26.1% | 27.6% | 24.0% |

| 2012-11-01 | 25.9% | 27.3% | 23.8% |

| 2012-12-01 | 25.7% | 26.8% | 24.3% |

| 2013-01-01 | 25.4% | 26.3% | 24.0% |

| 2013-02-01 | 25.2% | 25.9% | 24.2% |

| 2013-03-01 | 25.2% | 25.7% | 24.5% |

| 2013-04-01 | 25.1% | 25.4% | 24.7% |

| 2013-05-01 | 24.8% | 25.1% | 24.5% |

| 2013-06-01 | 25.0% | 25.3% | 24.5% |

| 2013-07-01 | 24.6% | 25.2% | 23.9% |

| 2013-08-01 | 24.8% | 25.3% | 24.2% |

| 2013-09-01 | 24.6% | 25.1% | 23.8% |

| 2013-10-01 | 24.3% | 25.1% | 23.3% |

| 2013-11-01 | 24.0% | 24.9% | 22.8% |

| 2013-12-01 | 23.4% | 24.3% | 22.2% |

| 2014-01-01 | 23.1% | 24.0% | 22.0% |

| 2014-02-01 | 23.0% | 24.1% | 21.4% |

| 2014-03-01 | 22.9% | 24.1% | 21.2% |

| 2014-04-01 | 22.5% | 23.9% | 20.5% |

| 2014-05-01 | 22.0% | 23.3% | 20.2% |

| 2014-06-01 | 21.4% | 22.5% | 19.8% |

| 2014-07-01 | 21.3% | 22.4% | 19.7% |

| 2014-08-01 | 20.6% | 21.7% | 19.0% |

| 2014-09-01 | 20.3% | 21.3% | 18.9% |

| 2014-10-01 | 20.1% | 20.8% | 19.0% |

| 2014-11-01 | 20.0% | 20.5% | 19.2% |

| 2014-12-01 | 19.9% | 20.6% | 19.0% |

| 2015-01-01 | 19.9% | 20.5% | 19.0% |

| 2015-02-01 | 19.8% | 20.1% | 19.3% |

| 2015-03-01 | 19.5% | 19.6% | 19.4% |

| 2015-04-01 | 19.3% | 19.3% | 19.3% |

| 2015-05-01 | 19.2% | 19.6% | 18.5% |

| 2015-06-01 | 19.0% | 19.6% | 18.2% |

| 2015-07-01 | 18.6% | 19.1% | 17.9% |

| 2015-08-01 | 18.5% | 18.8% | 17.9% |

| 2015-09-01 | 18.2% | 18.5% | 17.7% |

| 2015-10-01 | 17.9% | 18.1% | 17.6% |

| 2015-11-01 | 17.7% | 17.9% | 17.4% |

| 2015-12-01 | 18.0% | 18.1% | 18.0% |

| 2016-01-01 | 18.0% | 18.1% | 18.0% |

| 2016-02-01 | 17.9% | 18.0% | 17.8% |

* Data reflect 12-month moving averages; data for 2016 represent 12-month average from March 2015 to February 2016.

Note: Shaded areas denote recessions. Data are for high school graduates age 17–20 who are not enrolled in further schooling.

Source: EPI analysis of basic monthly Current Population Survey microdata

There are clear economic advantages for young people with a college degree relative to those who do not pursue and complete a college degree. This often leads pundits to suggest that more education is a solution to the low wages and high unemployment facing non-college educated workers. While this could be good advice at the individual level, encouraging more people to pursue higher education will do little to address the ongoing wage stagnation experienced by both high school and college graduates.

Weak productivity can be improved by full employment

Neil Irwin wrote a piece on productivity growth in the New York Times that’s making the rounds. It’s a good piece, definitely worth reading. But I think we need to focus a lot more on the portion of the productivity slowdown that is likely fixable quickly with policy: the depressing effect of chronic aggregate demand slack. While economics textbooks tend to shorthand the determinants of productivity growth as slow-moving, supply-side influences like the education of the workforce and the pace of technological advance, plenty of evidence shows that productivity growth is actually positively affected by the rate of demand-growth in the economy. If this is true, then the deceleration of productivity might be just the latest casualty from the too-long slog back to full recovery after the Great Recession. And this would in turn provide yet another reason why the Fed and other macro policymakers should err strongly on side of giving the economy too much rather than too little support going forward.

This theme—that productivity and potential output may be depressed by our failure to generate enough demand-growth to engineer a full recovery—is also a key point of my recent paper on the Congressional Progressive Caucus budget. If passed, this budget would do a lot for boosting productivity growth. People are absolutely right to be concerned about sluggish productivity growth, but we should at least try to pluck the low-hanging fruit in restoring a decent rate of growth by finally locking in full employment.

Restoring overtime will benefit millions of working people

For more than two years, the Obama administration has been working on restoring and strengthening working people’s right to receive overtime pay for working more than 40 hours per week. It’s been reported that the salary threshold under which all workers, regardless of their title or responsibilities, will be eligible for overtime will be set at $47,000 a year. While this is slightly lower than DOL’s original proposal, it represents a significant step forward in the effort to boost wages for working people.

If the salary threshold is indeed set at $47,000, it will directly benefit 12.5 million workers. 4.8 million workers will be newly eligible for overtime protections and another 7.6 million will be more easily able to prove their eligibility. All told, about 33 percent of the salaried workforce will be eligible for overtime, regardless of their duties on the job.

By restoring their right to be paid for the hours they work, President Obama and Secretary of Labor Perez are giving a raise to millions of working- and middle-class Americans. They deserve praise for their efforts.

Workers’ Memorial Day

On September 11, 2001, almost 3,000 people died in the attacks on the World Trade Center, the Pentagon, and the airliner crash in Pennsylvania. That tragedy is being compounded by the growing toll of cancer, lung disease and other illnesses related to the attack, particularly in the New York metro area, where first responders were exposed to a sickening mix of chemical and biological toxins. USA Today reported that “more than 9,000 claimants have been determined eligible for compensation of medical bills and other expenses,” and that 2,620 of the approved cases were cancer-related. This second wave of illness and death is taking place out of the public spotlight, but it is real and is causing suffering in thousands of families.

During the years since 9/11, a much larger wave of workplace deaths has been crashing down on American families without drawing much attention from the public or the media. Every year, more people are killed from injuries in the workplace than were killed on September 11, 2001. The number of fatal injuries has been as high as 5,840 but never lower than 4,551—this translates into roughly 65,000 unnecessary deaths resulting from negligence or the reckless indifference of employers who continue to send workers into unshored trenches, onto roofs without fall protection, into confined spaces filled with toxic gas, and into factories and mills with dangerous levels of explosive dust.

How bad are Trump’s policy instincts? He’s taking tax advice from Kansas governor Sam Brownback

In the last week, Donald Trump has backed away a bit from his ridiculous ideas to retire the federal debt by selling national assets and has noted his approval of the Federal Reserve’s low interest rate policies in recent years. This may have led some to question whether or not his policy instincts are really all that bad. They are.

To see why, one needs to dig into his plan for federal taxes. The regressiveness of this plan has been well-advertised: about 40 percent of the $9.5 trillion cut would eventually go to the top 1 percent. But look beyond this bullet point and you’ll see that Trump’s plan is so convoluted that a key loophole it contains has largely escaped analysis. This loophole is a piece of tax policy so bad that, at an Urban Institute panel on tax ideas from the campaign trail, Joe Rosenberg of the Tax Policy Center deemed it the worst tax idea from the campaign. To put it even more bluntly, this loophole is so bad that even the resolutely pro-tax cut Tax Foundation doesn’t like it.

Luckily, we already have evidence of just how bad this loophole is. This is because it has already helped blow a hole in the revenue of the only entity that has adopted it: the state of Kansas.

Tired of economists’ misdirection on globalization

An interesting story in the New York Times this morning looks at the effect that job losses from trade have had on people’s political views. It’s no surprise that voters on the losing end of globalization are disenchanted with the political mainstream, as the Times puts it. They have every right to be.

But I’m tired of hearing from economists about the failure to support workers dislocated by globalization as a cause of anger and the policy action the elite somehow mistakenly forgot. Ignoring the losers was deliberate. In 1981, our vigorous trade adjustment assistance (TAA) program was one of the first things Reagan attacked, cutting its weekly compensation payments from a 70 percent replacement rate down to 50 percent. Currently, in a dozen states, unemployment insurance—the most basic safety net for workers—is being unraveled by the elites. Only about one unemployed person in four receives unemployment compensation today.

I’m also getting tired of hearing that job losses from trade are the result of the U.S. economy “not adjusting to a shock.” Trade theory tells us that globalization’s impact is much greater on the wages of all non-college grads (who are between two-thirds and three-quarters of the workforce, depending on the year), not just a few dislocated manufacturing workers. The damage is widespread, not concentrated among a few. Trade theory says the result is a permanent, not temporary, lowering of wages of all “unskilled” workers. You can’t adjust a dislocated worker to an equivalent job if good jobs are not being created and wages for the majority are being suppressed. Let’s not pretend.

By failing to eliminate the tipped minimum wage, D.C. Mayor Bowser continues a legacy of inequality

This week, Washington, D.C. Mayor Muriel Bowser unveiled the details of her plan to raise the minimum wage in the District of Columbia to $15 an hour by 2020—unfortunately, the main difference between the Mayor’s plan and the ballot initiative is that her plan perpetuates the unjust subminimum wage for tipped workers.

Currently, tipped workers in the District are paid a minimum wage of just $2.77 an hour before tips and depend on diners to pay the bulk of their wages. Mayor Bowser’s proposal would raise the tipped minimum wage to $7.50 by 2024, where it would equal half the regular minimum wage. Having this separate, lower minimum wage for tipped works is unique to the United States; no other country has a separate minimum wage for tipped workers. This two-tiered system—which Mayor Bowser’s law will perpetuate—enshrines both gender and racial inequality directly into our labor law. The result is lower wages and higher levels of poverty for tipped workers, who are more often women and people of color.

When the first minimum wage was created in 1938 as part of the New Deal, it exempted many of the industries that commonly practiced tipping. The explicit subminimum wage for tipped workers was established in 1966 when the Fair Labor Standards Act was expanded, and restaurant owners and their lobbyists have defended the two-tier system ever since. The result is a subminimum wage for tipped workers that has been stuck at $2.13 at the federal level since 1991 and at $2.77 in DC since 1993.

This system has an obvious implication for working people who make their living in restaurants: they have lower wages and are much more likely to live in poverty. In states where tipped workers are paid a base wage of just $2.13 an hour, they are more than twice as likely to live in poverty than other workers. In these states, 18 percent of waitstaff and bartenders live in poverty, compared with 7 percent for other workers. In places like D.C., where tipped workers are paid a base wage somewhere between $2.13 and the full minimum wage, 14.4 percent of waitstaff and bartenders are in poverty.

Universities, inequality, and the overtime rule

The U.S. Department of Labor is about to issue a final rule that will increase the number of people entitled to overtime pay when they work more than 40 hours in a week. The rule will simply say, in effect, that if an employee earns less than $50,440 a year (or close to that—we won’t know the final number until the rule is released), she must be paid time and a half when she works more than 40 hours a week, even if she is a salaried employee, and even if her employer calls her a manager, professional, or supervisor.

This is a consequential move, which will improve the lives of many working people in a number of ways. Millions of employees who work long hours will get paid overtime for the first time. Millions of other workers who have been working long hours, at a cost to their health and their families, will have their hours reduced to 40 hours a week. Millions more will get a raise above the threshold, because their employer can continue to avoid paying overtime. And hundreds of thousands of people will get jobs because employers will reduce the hours of some employees to avoid paying overtime and hire additional people to do the work at straight time wages.

Many colleges and universities have complained that they cannot afford it. They don’t want to pay for overtime hours that have been free for years. At a congressional field hearing in March, the University of Michigan’s associate vice president for Human Resources said it would be “cost prohibitive” to raise salaries or pay overtime for post-doctoral researchers and others earning less than $50,000 a year. The coalition of universities and colleges lobbying to weaken the rule suggests a salary threshold “between $29,172 and $40,352” as the point where overtime pay could be denied. The U-M associate vice president went on to conclude that, “The climate for most colleges and universities in the U.S. is one of ongoing financial pressures that would curtail hiring new employees or increasing compensation as a result of these FLSA changes.”

Clarification on trade and American workers: right criticism, poorly targeted

It’s been pointed out to me that yesterday’s blog post about a story by NPR’s Chris Arnold targeted too much ire at Arnold himself rather than the phenomenon he was reporting about. I think that’s probably right, and so I apologize to him for that. I was using Arnold’s story as a jumping off point for a discussion of a larger issue, and should have made that more clear. I do think my larger points about the substance of the topic under debate hold. The damage done by trade to American workers is consistently underestimated and is often treated as a surprise when it shouldn’t be—it’s completely the prediction of standard trade theory. To the degree that Arnold’s story helps take this “surprise” excuse off the table for future debates over trade, it’s doing a service.

Some quick notes on why I think all of this is important, however. This is Arnold’s first paragraph:

Economists for decades have agreed that more open international trade is good for the U.S. economy. But recent research finds that while that’s still true, when it comes to China, the downside for American workers has been much more painful than the experts predicted.

I think Arnold reports this exactly right. Experts continue to portray the downside of expanded trade for American workers as having turned out to be unexpectedly large, but they are wrong to be surprised. Downward pressure on a large majority of American workers’ wages is completely predicted by mainstream economic theory. But I should have made clearer where my criticism here was aimed.

New legislation would bring transparency to America’s immigration system and help fight human trafficking

Every year, hundreds of thousands of workers from abroad come to the United States to temporarily fill jobs in a number of occupations, including farm labor, landscaping, hospitality and seafood processing, as well as information technology jobs or to teach at U.S. universities and grade schools. They come through a virtual alphabet soup of temporary foreign worker programs which are distinguished by different “nonimmigrant” visa classifications, each having their own distinct purpose and history. The most common nonimmigrant visas that authorize employment are the H-2A, H-2B, H-1B, J-1, L-1, A-3, G-5, F-1/Optional Practical Training (OPT), and B-1 visa classifications, but also important are H-1B1, O-1, O-2, E-2, E-3, P-1, P-2, Q-1, and TN visas. The workers themselves, who hold nonimmigrant visas, are commonly referred to as guestworkers and are allowed to remain and work in the country for a limited period of time, depending on the terms of their specific visa.

Over the years, countless cases of abuse and exploitation of guestworkers have come to light and been reported on by the media. The abuses are usually carried out by employers or the labor recruiters who connect guestworkers to their jobs and employers, for a fee. Some of the abuses are extreme and amount to human trafficking: they have been compared to slavery by Buzzfeed and the Southern Poverty Law Center and described as “creating an underground system of financial bondage” by the Center for Investigative Reporting. None of these labels are an exaggeration.

Unfortunately, little else is known about how these guestworker programs operate, despite the fact that hundreds of thousands of guestworker visas are issued every year. That makes it difficult to craft rational policy solutions to improve how the programs are managed and to ensure that the labor standards of guestworkers—and of Americans who work in major guestworker occupations—are protected. The dearth of information also results in an outsized role for corporate interest groups that spend millions lobbying to expand and deregulate guestworker programs, because it is difficult for lawmakers to verify claims about how guestworker programs impact the economy, businesses, and the labor market.

That’s why the Visa Transparency Anti-Trafficking Act, a new piece of legislation introduced today in the House by Reps. Lois Frankel (D-Fla.), David Schweikert (R-Ariz.), Ted Deutch (D-Fla.), and Jim Himes (D-Conn.), and in the Senate by Sen. Richard Blumenthal (D-Conn.), is so important. The Act would create a uniform system for reporting data that the government already collects on work visa programs and require making that information available to the the public, non-governmental organizations, researchers, and lawmakers. Because the government already possesses a vast amount of data on guestworker programs and temporary visas, the bill does not require the government to collect much more or to impose new burdens or requirements on employers. It would simply provide increased access to this information. That may seem like a small step, but it would go a long way to bringing a much-needed dose of transparency to our immigration system and drastically improve the quality of public debates surrounding temporary foreign worker programs.

It’s not a puzzle if American workers oppose trade agreements

Yesterday, NPR’s Chris Arnold wrote the latest in what has become a very long line of “explainer” pieces about economic globalization and the presidential campaigns. Nearly all of these pieces seek to resolve an alleged puzzle: nearly all reputable economists argue that policy efforts to boost trade are good for the U.S. economy, yet many (if not most) American workers strongly oppose trade agreements signed in recent decades.

Arnold puts forward a pretty common solution to this alleged puzzle: “trade’s benefits are diffuse, but the pain is concentrated.” In this view, the only losers from trade are those workers directly displaced by imports. Every other consumer in the economy benefits from lower prices. But because the losers are small and concentrated, they can organize to oppose trade agreements. And while the winners are numerous and widespread, the benefits (e.g., slightly more affordable clothing and DVD players) are hard to notice, so no one organizes to support these agreements.

This is a common way of describing the effects of using policy to expand trade, but on the economics, it is certainly not correct. In textbook trade models, using policy levers (lower tariffs, for example) to boost trade with poorer countries will indeed cause total national income in the United States to rise. But these same textbooks also predict that the resulting expansion of trade will redistribute far more income than it creates. And the direction of this redistribution is upward. So it is perfectly possible to have policy efforts to expand trade lead to higher national income yet leave the majority of workers worse off. Importantly, the losers in these textbook models are not just workers directly displaced by imports—they’re all the workers in the entire economy who resemble the trade-displaced in terms of education and credentials.

U.S. trade policy: Populist anger or out-of-touch elites?

This post originally appeared in The Globalist.

The presidential primary campaigns of both political parties have exposed widespread voter anger over U.S. global trade policies. In response, hardly a day has recently gone by without the New York Times, the Washington Post and other defenders of the status quo lecturing their readers on why unregulated foreign trade is good for them. The ultimate conclusion is always the same—that voters should leave complicated issues like this to those intellectually better qualified to deal with them. Trade experts, according to Binyamin Appelbaum of the Times have been “surprised” at the popular discontent over this issue. Their surprise only shows how disconnected the elite and the policy class that supports it is from the way most people actually experience the national economy. The United States has always been a trading nation. But until the 1994 North American Free Trade Agreement, trade policy was primarily an instrument to support domestic economic welfare and development.

A lop-sided deal: Investment vs. jobs

Starting with NAFTA, pushed through not by a Republican president, but by the Bill Clinton in 1994, it became a series of deals in which profit opportunities for American investors were opened up elsewhere in the world in exchange for opening up U.S. labor markets to fierce foreign competition. As Jorge Castañeda, who later became Mexico’s foreign minister, put it, NAFTA was “an agreement for the rich and powerful in the United States, Mexico and Canada, an agreement effectively excluding ordinary people in all three societies.” For 20 years, leaders of both parties have assured Americans that each new NAFTA-style deal would bring more jobs and higher wages for workers, and trade surpluses for their country. It was, they were told, an iron law of economics.

Paul Ryan failed to pass a Republican budget resolution—but that’s good news

It’s now widely accepted among Washington commentators that the Republican House of Representatives dropped the ball on the federal budget over the past week. You might think this means people have finally noticed just how bad the Republican House Budget Resolution that passed out of committee recently was. But, no.

Instead, the tsk tsking is about the Republicans officially missing the statutory deadline to pass a budget resolution. Now, this is a puzzling failure, to be clear. Republicans have majorities in both the House and the Senate, and Speaker Paul Ryan promised to restore “regular order” on budgets during his tenure.

And Republicans had fun in recent years characterizing Democrats as not doing their jobs because they could not pass annual budgets through regular order (the irony, of course, being that these budgets were held up by Republicans boisterously opposing any compromise). Mitch McConnell did some of the best mocking, “I don’t think the law says, ‘Pass a budget unless it’s hard,’ so I think there’s no question that we would take up our responsibility. We would be passing a budget. Every year.”

On renaming the Woodrow Wilson School: The standards of his time, and ours

Last week, the Princeton University trustees announced they were rejecting student protester demands that “Woodrow Wilson” be removed from the names of the university’s School of Public and International Affairs and a residential undergraduate college.

The protesters objected to honoring Wilson because he participated in and, as president of the United States, helped lead a national wave of reaction against the progress towards equality that African Americans had made in the decades after emancipation. In particular, Wilson segregated, for the first time, the federal civil service.

The trustees agreed that Wilson’s racial policies, both as president of the university (where he refused to admit African American students) and as president of the United States were a serious blemish on his record. They recommended greater efforts to recruit African American students, programs to better incorporate those students into university life, and “a much more multi-faceted understanding and representation of Wilson on our campus, especially at the school and the college where his name is commemorated.” They made no specific proposals in this regard, but it would seem reasonable to install a prominent plaque at the entrances of these buildings that describe Wilson’s contributions to segregating American society, and distribute a pamphlet to each student at the school and college that describes the origins of segregation and Woodrow Wilson’s contribution to it.

Such an approach would be preferable to removing his name. Preserving the identity of the school and college should be a provocation for ongoing discussion of this history. Sanitizing the names, in contrast, could ensure that future generations of Princeton students will be as little challenged by that history as previous generations have been.

TIME runs incoherent rant on U.S. debt as cover story

After a too-short hiatus, fear-mongering about the debt is back in a big way. TIME magazine is so worried that they’ve taken it upon themselves to not only put out an entire series to remind people that they must still fear the debt boogeyman, but have also allowed the headline story to center on long-debunked ramblings about the glories of the gold standard. There is so much wrong in the headline story that it would take a treatise to correct, but let’s just focus on a couple of easy things.

First: $13,903,107,629,266 (the size of the federal government’s debt)—that’s a big number. But context, one of many things lacking in this article, is also important. $18,164,800,000,000 is a larger number, and one that happens to be U.S. Gross Domestic Product (GDP). As was highlighted in our recent piece on Donald Trump, what matters is the size of public debt relative to the size of the economy. For further context, Greek debt at its recent peak was 175 percent of Greek GDP. That’s a level that the Congressional Budget Office baseline doesn’t even have the U.S. government hitting in three decades. And even Greek debt had to be combined with screaming policy incompetence among European Union policymakers to spark an economic crisis. Finally, if we believe that the confidence fairy may tolerate a couple of years of deficits but will come roaring back to punish us because of sustained debt levels, then it’s worth noting that Japan, where debt currently sits at 123 percent of GDP, has had a debt-to-GDP ratio of over 80 percent since 2004—with no signs yet of creditors fleeing.

Since the author of the TIME article, James Grant, is determined to analogize between government debt and personal debt, we should point out a couple of quick things. First, even for a person, a debt that is less than 80 percent of their annual income is far from ruinous. Lots of Americans would, for example, rejoice if their outstanding mortgage was less than 80 percent of their annual salary. Second, lots of people have debts—mortgages, auto loans, student loans—and yet have substantial net worth because they also own assets. Both of these insights apply to the government, maybe even more forcefully. For example, many people with mortgages less than 80 percent of their annual income would consider themselves in a good financial place. But people really do have to pay off their mortgage in full someday. Governments—entities that never die—don’t. So, the burden of an 80-percent-of-income debt is much, much less pressing to a government than a person. The government also owns assets. Lots of them. And these estimates of assets don’t even include the biggest one: the power to tax.

There are economically coherent arguments about why the United States should address projected future deficits before too long. They’re not hugely convincing to us, but they do exist. But they’re not in the new TIME magazine cover story.

Verizon shows us why strikes—and unions—matter for working people

40,000 Verizon workers are currently on strike across the country after the company and labor unions failed to reach a new contract agreement last year. Verizon has reaped over $39 billion in profits over the last three years, and its CEO rakes in 200 times more per year than the average Verizon worker. Despite this clear sign of prosperity, Verizon refuses to let its employees share these gains. Instead, Verizon wants to severely cut health care coverage, slash benefits for injured and retired workers, and outsource work to low-wage contractors overseas. As the daughter of a striking Verizon worker and as a union member myself, I know that workers do not decide lightly to go on strike. Strikes are disruptive and stressful, and create financial strain for workers and their families. But they are necessary when large corporations refuse to give working people a fair share of the profits they help create, and Verizon workers have been without a contract for ten months.

By going on strike, the Verizon workers are using one of the few tools workers have left in today’s economy to claim their fair share of economic growth. They are also pushing back against the rigged rules of the economy that privilege capital owners and corporate managers. I stand in solidarity with my mother and thousands of her fellow union members as they fight for a fair contract. Their call for job security, protected benefits, and improved working conditions is emblematic of larger trends affecting working people across America. Their strike is also an example of how important it is for working people to have the right to stand together and negotiate collectively for fair wages and benefits and safe working conditions. Unfortunately, this right has been severely eroded over the fifty years by policy choices made on behalf of those with the most wealth and power—and this erosion has directly contributed to stagnating wages for the vast majority of workers.

Wisconsin’s so-called right to work law has been ruled unconstitutional

A trial court in Wisconsin has ruled that the state’s new law banning union contracts that make every employee the union represents pay his fair share of the costs of representation is unconstitutional.

The union plaintiffs and the court took a fairly novel approach to this issue and ruled on grounds I had never considered: compelling a union to represent non-dues-paying free riders (as the law does) means the state is taking the union members’ dues and forcing them to spend it on free riders without any compensation by the state. It’s an unconstitutional taking without just compensation, in violation of Article 1, section 13 of the Wisconsin constitution. A similar argument under the Fifth Amendment of the U.S. Constitution was made by Judge Diane Wood, dissenting in Sweeney v. Pence, 767 F3d 654, 683-84 (7th Cir 2014), where the majority upheld Indiana’s identical law.

The state requires unions to represent every member of the bargaining unit fairly and equally, so the union can’t avoid spending from its treasury when a non-dues-payer demands that the union take his grievance, in a situation where it would take a union member’s grievance. That representation can involve arbitration fees and the costs of a lawyer, which can easily exceed $10,000. The state imposes this burden on the union for the “public purpose [of] making the business climate in the state more favorable,” but it offers the union no compensation at all. The court rejected the notion that giving the union exclusive bargaining rights was sufficient compensation: “The proposition that winning an election is sufficient compensation and that all subsequent work must be done for free does not make any more sense than the proposition that there is a free lunch.”

Trump’s debt proposal is a mix of conventional and unconventional stupidity

Over the weekend, Republican presidential candidate Donald Trump insisted that he could eliminate the national debt, which currently stands at around $19 trillion, “over a period of eight years.” Upon hearing this, most people would think that Trump planned to cut spending or hike taxes. However, Trump plans to cut taxes, which suggests that he had to be proposing enormous spending cuts. If spending cuts began rapidly enough to fulfill Trump’s promise of eliminating our $19 trillion debt, the “very massive recession” that is currently just another of Trump’s fantasies would become a very real possibility.

Trump, however, has something else in mind besides (or at least in addition to) spending cuts as a strategy for eliminating our national debt. Trump’s plan is a relatively new twist in D.C. policy debates: selling government assets.

This plan, while truly stupid, is a useful reminder about how limited and silly our budget deficit debates are in D.C. While it has received plenty of deserved scorn, we shouldn’t lose sight of the fact that about half of the ridiculousness of Trump’s overall debt plan actually just mimics pretty conventional D.C. budget wisdom. The other half brings a new kind of ridiculousness to the table, but these new proposals come with a grain of useful insight embedded in them. First, though, it will help to examine the conventional ridiculous featured in Trump’s plan.

First, there is the $19 trillion debt number that Trump references. Anybody who tells you the national debt is $19 trillion is simply fear-mongering. This $19 trillion number is the gross national debt, which includes debt issued to government accounts (in practice, this means debt held by the Social Security Trust Fund). According to the Congressional Budget Office (CBO), this debt “does not directly affect the economy and has no net effect on the budget.” What matters for future taxpayers is the net debt (i.e., the debt held by the public), which CBO’s most recent measure puts at about $13 trillion in 2015. $13 trillion should be a big-enough number to sound scary, but D.C. budget fear-mongers can never resist going for the even higher (though irrelevant) $19 trillion.

Putting things in perspective: Bernie Sanders, trade, and poor countries’ access to U.S. markets

Yesterday, Zack Beauchamp updated a piece he had written a while back that claimed Bernie Sanders’ trade agenda could prove ruinous to the world’s poorest people. I think Beauchamp really overstates this, for a couple of reasons.

First, only an expansive reading of some of Sanders’ rhetorical excesses would lead one to think he would pursue policies that radically restricted the access to U.S. markets currently enjoyed by our poorer trading partners’ exports. It is not an uncommon reaction to criticisms of today’s global trade regime to assume that this market access would clearly be significantly reduced if this status quo were overturned, but that’s far from obvious.

Second, the evidence marshalled on behalf of trade liberalization’s positive benefits for development is entirely about the benefits of unilateral, domestic liberalization. That is, the benefits a country gains from cutting its own tariffs, and not about the ease of access that they have to the U.S. market. This evidence is completely silent on the benefits of access to the U.S. market. Economic theory teaches that the benefits of unilateral liberalization completely dwarf those of market access, and there is not much evidence to suggest that this theory is wrong.

Commonsense rule to protect investors from conflicted advice survives industry onslaught

A rule requiring investment advisors to act in the best interest of clients saving for retirement was released today despite a six-year campaign to weaken or kill it. Secretary of Labor Thomas Perez and his staff deserve enormous credit for persevering.

The financial services industry made the usual claim that the rule would hurt the people it was supposed to help—essentially, that investors are better off with bad advice than no advice. It also told Congress the rule would be unduly burdensome, while assuring investors there was nothing to worry about, as Senator Elizabeth Warren and Representative Elijah Cummings pointed out.

Let’s hope the financial industry was lying to investors, not Congress, because the rule should have an impact on its bottom line. The only problem is that it doesn’t go far enough. A financial advisor can now be sued for recommending a higher-cost mutual fund over a similar but lower-cost fund without disclosing that he or she is working on commission—a practice that was perfectly legal until today. But the rule doesn’t require that he or she provide information about low-cost index funds and similar investments, even though the original draft rule pointed out that the prevailing view in the academic literature was that such a passive investment strategy was optimal.

It’s unlikely that investors could successfully sue advisors simply for steering them to higher-cost asset classes, as long as the investments are generally considered suitable for people saving for retirement (mutual funds or annuities, for example, and not shares in racehorses). But the mutual fund and insurance industries succeeded in having this spelled out in the final rule and eliminating a safe harbor for broker-dealers offering “high-quality low-fee products… calibrated to track the overall performance of financial markets.” The list of other changes is worth reading and perhaps worrying about, though they may matter little in practice and simply allow the administration to demonstrate its responsiveness while giving lobbyists something to show for their expensive efforts.