The Fed shouldn’t give up on restoring labor’s share of income—and measure it correctly

U.S. workers’ wages have climbed modestly but noticeably over the past year. EPI’s nominal wage tracker shows that in 2015 and 2016, this growth averaged 2.4 percent, in 2017 it averaged 2.5 percent, but in 2018 it accelerated to 2.85 percent—and it surpassed 3 percent growth in the last quarter of the year. This uptick has been long-coming and it took a longer spell of low unemployment to spur it than most would have thought.

Three percent growth for a quarter, however, should not constitute “mission accomplished” in the minds of macroeconomic policymakers like the Federal Reserve. In the long run, nominal wage growth should run at a rate equal to the Fed’s inflation target (2 percent) plus the long-trend growth in potential productivity (let’s call this 1.5 percent).1 This indicates that even the recent accelerations in wage growth leave us failing to meet these long-run goals.

Even more importantly, wage growth should run substantially above these long-run targets for a spell of time after long periods of labor market slack. The arithmetic reasoning for this is straightforward: any time wage growth runs slower than current rates of inflation plus productivity, the result will be labor compensation shrinking as a share of the economy. The economic intuition is simply that extended periods of labor market slack sap workers’ ability to secure wage increases from employers.

This undermining of labor’s leverage shows up clearly in the data. EPI’s nominal wage tracker, besides charting wage growth over time, also tracks a measure of labor’s share of income, precisely to highlight the accumulated shortfall of labor income that policymakers should aim to restore.

What to Watch on Jobs Day: Furloughs and month-to-month volatility

The government shutdown adds several layers of complexity to interpreting January employment figures set for release on Friday. While I still plan to look at wage growth and the prime-age employment-to-population ratio to measure the slack that remains in the labor market, the effect of the extended partial government shutdown on the top-line employment numbers will get a lot of attention too. In this post, I will explore how the shutdown likely will and will not affect the numbers, along with a reminder about typical month-to-month volatility.

The reference period for the upcoming Current Employment Statistics (CES) and the Current Population Survey (CPS) is the pay period or week, respectively, including January 12, 2019. The 12th of January marks roughly the middle of the 35-day partial government shutdown. The shutdown directly affected three types of workers and their paychecks: government employees working without pay, government employees not working, and government contractors not working. Indirectly, the shutdown also affected workers who typically service government employees who were not working, but who are not directly paid for by government contracts—think restaurants, taxi cabs, and other services purchased by the government workforce.

Let’s start with the CES. Government workers, furloughed or not, will be counted as employed in the CES. As soon as the Government Fair Treatment Act of 2019 was signed into law, those furloughed workers were guaranteed their back pay and therefore count as employed workers. In other words, the effects of the furlough will not affect the count of federal jobs in the CES. The loss of private sector work, on the other hand, either as direct federal contractors or indirect employment that services government work, could register as a fall in private-sector employment or private-sector hours, or both.

The number of unionized U.S. workers edged lower to 16.4 million in 2018

The number of American workers represented by a labor union ticked down last year, extending a decades-long trend.

New data on union membership from the Bureau of Labor Statistics released on Friday showed 16.38 million unionized workers in 2018, down from 16.44 million in 2017. However, because employment of wage and salary workers grew by 1.6 percent between 2017 and 2018, the share of workers represented by a union declined by a more significant amount, from 11.9 percent to 11.7 percent.

In the private sector, the number of workers represented by a union ticked up slightly (+18,000). But due to the 1.7 percent increase in employment in the private sector, the share of private sector workers represented by a union declined, from 7.3 percent to 7.2 percent.

The losses were greater in the public sector. The number of public sector workers represented by a union declined by 83,000, while the share of public sector workers represented by a union declined by seven-tenths of a percentage point, from 37.9 percent to 37.2 percent. The drop was largest at the state government level, with the share of state government workers represented by a union dropping from 33.4 percent to 31.8 percent.

Reliable data is one of the many victims of the government shutdown

One of the many things we rely on the federal government for is timely, accurate, independent, and publicly available data that is used by households, businesses, and policymakers to make informed economic decisions. Of the many negative effects of the government shutdown, there have been some “data casualties,” including the release of Current Population Survey (CPS) public microdata files. These files are the source data for monthly reports on the unemployment and labor force participation rates, key timely barometers of the nation’s economic health. This microdata also forms the basis of much of the research that EPI and other research organizations and academics conduct. EPI urges the president to end the government shutdown so that federal employees and contractors can receive their paychecks again, researchers at EPI and elsewhere can continue to provide current economic analysis, businesses and households can make economic plans with fuller information, and the new Congress can make well-researched policy choices.

The Current Population Survey (aka the Household Survey), which is used to measure the nation’s unemployment rate (along with many other measures of labor market health), is collected and analyzed through a partnership between the Bureau of Labor Statistics (BLS) and the Census Bureau. Every month, a few weeks after BLS releases the monthly jobs report with CPS-derived estimates of unemployment and labor force participation, Census releases a version of the CPS microdata for public use. These public-use extracts allow for analysis beyond what’s available in tables published by BLS. For example, the jobs report includes an enormous amount of information on employment status by race/ethnicity, gender, age, education, and a variety of other demographic characteristics. However, to look at how the employment status of young people with a high school degree differs by race, you need to use the CPS microdata to run your own analysis. The CPS microdata is also a key source for assessing trends in wage growth for workers at different points in the wage distribution—an assessment we make annually at EPI and which will be delayed by this week’s announcement.

Au pair lawsuit reveals collusion and large-scale wage theft from migrant women through State Department’s J-1 visa program

Last week, the Associated Press (AP) reported on a proposed settlement agreement for $65.5 million between a dozen former au pairs from Colombia, Australia, Germany, South Africa, and Mexico who were brave enough to bring a lawsuit against the companies that recruited them to work the United States. Thanks to the former au pairs and the tireless efforts of the smart lawyers at Towards Justice, a nonprofit organization in Denver, nearly 100,000 young migrant workers (mostly women) will finally receive some portion of the wages they should have been paid while working in the United States providing low-cost child care to Americans.

The migrant au pairs doing this work as in-home caretakers were employed in the United States through the U.S. State Department’s Au Pair program, one of 15 programs in State’s J-1 visa Exchange Visitor Program. Each year about 20,000 au pairs are hired by American families, assisted by J-1 “sponsors,” which can be either for-profit companies or nonprofit organizations that act as labor recruiters for families looking to hire foreign au pairs, and to which the State Department has mostly outsourced the management and oversight of the J-1 visa program. The sponsors make money by charging the au pairs to participate in the program, as well as by charging fees to families in order to connect them to au pairs. According to the AP, in the lawsuit the au pairs claimed that the:

15 companies authorized to bring au pairs to the United States colluded to keep their wages low, ignoring overtime and state minimum wage laws and treating the federal minimum wage for au pairs as a maximum amount they can earn. In some cases, the lawsuit said, families pushed the limits of their duties, requiring au pairs to do things like feed backyard chickens, help families move and do gardening, and not allowing them to eat with the family.

The economy has made great strides since the recession, but some weakness lingers

With today’s Bureau of Labor Statistics (BLS) jobs report we can look at the entirety of 2018—putting the year as a whole in perspective and comparing 2018 with other years. Yesterday, I provided a fairly broad overview of the first 11 months of 2018 including context since the last business cycle peak before the Great Recession (2007) and the last time the U.S. economy was at full employment (2000).

As the recovery has strengthened we’ve seen improvements in all measures of employment, unemployment, and wage growth. These measures tell a consistent story—an economy on its way to full employment, but not there yet. Taking a data-driven approach to policymaking would mean continuing to push to reduce slack, keeping interest rates from rising further and letting the economy recover for Americans across races, ethnicities, ages, levels of educational attainment, and areas of the country.

Payroll employment growth in December was 312,000, bringing average job growth in 2018 up to 220,000. As shown in the figure below, job growth during this time period was a bit higher than in 2017. This can be attributed to the shift in federal policy from austerity to stimulus in the form of both tax cuts and a nearly $300 billion increase in government spending.

Average monthly total nonfarm employment growth, 2006–2018

| Year | Average monthly total nonfarm employment growth |

|---|---|

| 2006 | 175 |

| 2007 | 96 |

| 2008 | -297 |

| 2009 | -422 |

| 2010 | 88 |

| 2011 | 174 |

| 2012 | 179 |

| 2013 | 192 |

| 2014 | 250 |

| 2015 | 226 |

| 2016 | 195 |

| 2017 | 182 |

| 2018 | 220 |

Source: Data are from the Current Employment Statistics (CES) series of the Bureau of Labor Statistics and are subject to occasional revisions.

What to Watch on Jobs Day: An assessment of the 2018 labor market, 11 years since the start of the Great Recession

The last Bureau of Labor Statistics (BLS) jobs report of 2018 comes out on Friday, giving us a chance to step back and look at how working people fared over the entire year. The report also marks the 11th anniversary of the official start of the Great Recession. My expectation is that the December data will confirm that, while by some measures the economy has nearly recovered its immediate pre-Great Recession health, by other measures it is still somewhat weaker than in 2007—the last year before the Great Recession hit. Further, as I have often noted, 2007 should not be considered a benchmark for a fully healthy economy for America’s workers. Almost all labor market measures were notably weaker in 2007 than they were at the previous business cycle peak in 2000. There was very little reason to think that the U.S. economy in 2007 was at full employment. If one looks at the stronger business cycle peak of 2000 as a more appropriate benchmark, the economy in 2018 looks even further from full employment. Many working people are still not seeing the recovery reflected in their paychecks—and the economy will not be at genuine full employment until employers are consistently offering workers meaningfully higher wages.

In this blog post—and Friday when the December numbers come out—I’m going to look at average payroll employment growth over the last several years. Because there is always a bit of volatility in the monthly data—especially in the household series that has a smaller sample size—taking a year-long approach allows us to smooth out the bumps and take stock of the key measures: payroll employment growth, the unemployment rate, the employment-to-population ratio, and nominal wage growth.

Over 5 million workers will have higher pay on January 1 thanks to state minimum wage increases

On January 1, 2019, 19 states will raise their minimum wages, lifting pay for 5.2 million workers across the country.1 The increases, which range from a $0.05 inflation adjustment in Alaska to a $2.00 per hour increase in New York City, will give affected workers approximately $5.3 billion in increased wages over the course of 2019. Affected workers who work year-round will see their annual pay go up between $90 and $1,300, on average, depending on the size of the minimum wage change in their state.

The map below describes the impacts of each state increase, which are also summarized in Table 1. Note that these estimates do not account for changes in local minimum wages.2 There are 24 cities and counties with higher local minimum wages taking effect on January 1, all of which can be found in EPI’s Minimum Wage Tracker. They also do not include any “indirectly affected workers” already making more than the new minimum wage who receive raises as employers adjust their overall pay scales.

Increases in eight states are the result of automatic adjustments for inflation. In Alaska, Florida, Minnesota, Montana, New Jersey, Ohio, South Dakota, and Vermont, the minimum wage is adjusted each year to reflect changes in prices over the preceding year—thereby ensuring that the minimum wage supports the same level of spending year after year.

In five states—California, Delaware, Massachusetts, New York, and Rhode Island—the increases reflect new minimum wage levels set by state legislatures. Several of these increases, such as those in California, Massachusetts, and New York, are intermediate steps as these states gradually raise their minimum wages to $15 per hour. In 2017, congressional Democrats proposed raising the federal minimum wage to $15 by 2024, which would lift pay for an estimated 41 million U.S. workers, but the bill was never allowed to come to a vote. Lawmakers in Congress have not raised the federal minimum wage since 2007, and since the last federal increase took effect, the purchasing power of the federal minimum wage has declined by over 12 percent.

The failure of Trump’s trade and manufacturing policy

A shorter version of this post appeared in the Detroit News on 12/2/2018: GM Cutbacks a result of overvalued dollar.

Last month, General Motors announced plant closures in the U.S. that could lead to roughly 14,700 layoffs by the end of 2019. The shutdowns will have the biggest impact in industrial states like Ohio and Michigan, where key plants in Detroit-Hamtramck, Lordstown, and Warren are being closed. But the closures also have wider implications for American industry—and not just the machine shops and fabricators that produce rubber, steel, and glass components for auto assembly. America’s manufacturers are all struggling with the same issue—an overvalued dollar that puts them at risk from rising trade deficits. And it all derives from flawed Trump administration economic policies.

Trump’s tax cuts and increased government spending for defense and nondefense needs are widening the U.S. budget deficit, which will top $1 trillion in 2020 (5 percent of GDP). On top of that, Trump’s tariffs on China have backfired. China has reduced the value of the yuan 10 percent this year, and its trade surplus with the United States has increased 10 percent over the same period last year—even faster than the overall U.S. goods trade deficit, which is up 9.4 percent in the same period. The IMF projects that the overall U.S. current account deficit (the broadest measure of trade in goods, services and income) will nearly double over the next four years.

As a result of the rising dollar and increasing current account deficit, the U.S. goods trade deficit will increase to between $1.2 trillion and $2 trillion by 2020, an increase of $400 billion to $1.2 trillion above the $807 billion U.S. goods trade deficit in 2017, as shown below. This will directly eliminate between 2.5 and 7.5 million U.S. jobs, mostly in manufacturing (because 85 percent of U.S. goods trade consists of manufactured products). The collapse in output, especially in the capital intensive manufacturing sector, will decimate investment—and taken together, both will result in large additional job losses as income and spending collapse, resulting in a steep recession if nothing is done to reduce the over-valued dollar. The dollar must fall by at least 25 to 30 percent (on a real, trade-weighted basis) to rebalance U.S. trade and avert the coming trade tsunami that’s baked into the economy as a result of the rising trade deficit.

The bad economics of PAYGO swamp any strategic gain from adopting it

The obscure Congressional budget rule known as PAYGO (“pay as you go”) has burst into the news lately. A PAYGO rule means that any tax cut or spending increase passed into law needs to be offset in the same spending cycle with tax increases or spending cuts elsewhere in the budget. Incoming House Speaker Nancy Pelosi has indicated that the House of Representatives will abide by PAYGO in the next Congress, and this decision has sparked much controversy.

Many Washington insiders assert forcefully that committing to PAYGO rules in the House for the next Congress is good politics. The argument is that it assuages fears of politicians who believe they must make public commitments to lower deficits to avoid being punished by voters who care deeply about this issue. If voters do indeed have strong preferences for reducing deficits, then policymakers—even those who want to use fiscal policy to reduce inequality by expanding public spending and investment—must first commit to PAYGO to convince these voters that budget measures can both reduce inequality and be fiscally “responsible.”

The strength of evidence supporting this political claim is debatable. What’s less debatable is that PAYGO really has hindered progressive policymaking in the not-so-recent past. For example, it was commitments to adhere to PAYGO that led to the Affordable Care Act (ACA) having underpowered subsidies for purchasing insurance and, even more importantly, having a long lag in implementation; the law passed in January 2010 yet the exchanges with subsidies only were up and running by 2014. This implementation lag meant that the ACA’s benefits were not as sunk into Americans’ economic lives by the time a hostile Republican Congress and administration began launching attacks on it following the 2016 elections. It is a real testament to how much better the ACA made life for Americans that it has been stubbornly resistant to these attacks. But it would have been helpful to have a couple more years to have it running smoothly, but that didn’t happen largely because the ACA’s architects wanted to meet PAYGO rules over the 10-year budget window.

Bonuses are up $0.02 since the GOP tax cuts passed

Newly available data from the Bureau of Labor Statistics’ Employer Costs for Employee Compensation data allows an update of the trends of worker bonuses through September 2018, to gauge the impact of the GOP’s Tax Cuts and Jobs Act of 2017. The tax cutters claimed that their bill would raise the wages of rank-and-file workers, with congressional Republicans and members of the Trump administration promising raises of many thousands of dollars within ten years. The Trump administration’s chair of the Council of Economic Advisers argued in April that we were already seeing the positive wage impact of the tax cuts:

A flurry of corporate announcements provide further evidence of tax reform’s positive impact on wages. As of April 8, nearly 500 American employers have announced bonuses or pay increases, affecting more than 5.5 million American workers.

Following the bill’s passage, a number of corporations made conveniently-timed announcements that their workers would be getting raises or bonuses (some of which were in the works well before the tax cuts passed). But as Josh Bivens and Hunter Blair have shown there are many reasons to be skeptical of the claim that the TCJA, particularly corporate tax cuts, will produce significant wage gains.

Millions of working women of childbearing age are not included in protections for nursing mothers

The federal Break Time for Nursing Mothers provision of the Fair Labor Standards Act (FLSA) requires employers to provide reasonable unpaid break time, as needed, for an employee to express breast milk for her nursing child for one year after the child’s birth. Further, employers are required to provide a place for the employee to express milk—other than a bathroom—that is shielded from view and free from intrusion from coworkers and the public. These requirements were signed into law in 2010 as part of the Affordable Care Act and were a landmark step toward securing pumping accommodations for countless nursing mothers in the workplace.

These provisions were designed to prevent harmful outcomes that can occur without basic workplace accommodations for expressing breast milk, such as negative health consequences, the inability to breastfeed, and economic harm including job loss (documented in the upcoming report Exposed: Discrimination Against Breastfeeding Workers from the Center for WorkLife Law). However, the law has several significant problems that leave nursing mothers at risk. One key issue is that due to where these provisions are placed in the FLSA—in the section that requires employers to pay overtime compensation if an employee works more than 40 hours in a week—all those workers who are exempt (i.e. excluded) from the overtime protections of the FLSA are also exempt from the break time protections for nursing mothers. These exemptions affect roughly one out of every four working women of childbearing age (between the ages of 16 and 44). There are a total of 37.8 million working women of childbearing age in the United States, and more than 9 million of them are excluded from the Break Time for Nursing Mothers protections. That includes more than 1 million black women, 976,000 Hispanic women, 825,000 Asian women, more than 6 million white women, and 185,000 women of other races. The below table shows further breakdowns by state and industry.

What to Watch on Jobs Day: Will we see signs of stronger wage growth?

Friday is the last Bureau of Labor Statistics (BLS) Jobs Report before the final meeting of the year for the Federal Open Market Committee (FOMC) meeting. The FOMC has a dual mandate to pursue both maximum employment as well as stable inflation around their 2 percent target. Current forecasts signal that it’s more likely than not that the FOMC will raise interest rates in their December meeting, on pace with their behavior this year so far. However, the data, should give them pause to hold off and let the economy continue to recover—and the data they should really be paying attention to comes from the labor market, not the stock market.

While the economy is experiencing continued low unemployment, there’s other evidence to suggest that recent levels of unemployment are overstating the strength of the economy. The share of the population with a job continues to be softer than recent labor market peaks. The figure below shows the share of the 25–54 year old population with a job, removing any issues of a shrinking labor force due to retiring baby boomers. This prime-age employment-to-population ratio most recently came in at 79.7 percent, a huge improvement since the depths of the aftermath of the Great Recession, but still more than 2 percentage points lower than when the economy was closest to full employment back in 2000.

Employment-to-population ratio of workers ages 25–54, 1989–2024

| date | Employment to population ratio |

|---|---|

| Jan-1989 | 80.0% |

| Feb-1989 | 79.9% |

| Mar-1989 | 79.9% |

| Apr-1989 | 79.8% |

| May-1989 | 79.8% |

| Jun-1989 | 79.8% |

| Jul-1989 | 79.8% |

| Aug-1989 | 79.9% |

| Sep-1989 | 80.0% |

| Oct-1989 | 79.9% |

| Nov-1989 | 80.2% |

| Dec-1989 | 80.1% |

| Jan-1990 | 80.2% |

| Feb-1990 | 80.2% |

| Mar-1990 | 80.1% |

| Apr-1990 | 79.9% |

| May-1990 | 79.9% |

| Jun-1990 | 79.8% |

| Jul-1990 | 79.6% |

| Aug-1990 | 79.5% |

| Sep-1990 | 79.4% |

| Oct-1990 | 79.4% |

| Nov-1990 | 79.2% |

| Dec-1990 | 79.0% |

| Jan-1991 | 78.9% |

| Feb-1991 | 78.9% |

| Mar-1991 | 78.7% |

| Apr-1991 | 79.0% |

| May-1991 | 78.6% |

| Jun-1991 | 78.7% |

| Jul-1991 | 78.6% |

| Aug-1991 | 78.5% |

| Sep-1991 | 78.6% |

| Oct-1991 | 78.5% |

| Nov-1991 | 78.4% |

| Dec-1991 | 78.3% |

| Jan-1992 | 78.4% |

| Feb-1992 | 78.2% |

| Mar-1992 | 78.2% |

| Apr-1992 | 78.4% |

| May-1992 | 78.4% |

| Jun-1992 | 78.5% |

| Jul-1992 | 78.4% |

| Aug-1992 | 78.4% |

| Sep-1992 | 78.3% |

| Oct-1992 | 78.2% |

| Nov-1992 | 78.2% |

| Dec-1992 | 78.2% |

| Jan-1993 | 78.2% |

| Feb-1993 | 78.1% |

| Mar-1993 | 78.2% |

| Apr-1993 | 78.2% |

| May-1993 | 78.5% |

| Jun-1993 | 78.6% |

| Jul-1993 | 78.6% |

| Aug-1993 | 78.8% |

| Sep-1993 | 78.6% |

| Oct-1993 | 78.7% |

| Nov-1993 | 79.0% |

| Dec-1993 | 79.0% |

| Jan-1994 | 78.9% |

| Feb-1994 | 78.9% |

| Mar-1994 | 78.9% |

| Apr-1994 | 79.0% |

| May-1994 | 79.2% |

| Jun-1994 | 78.8% |

| Jul-1994 | 79.1% |

| Aug-1994 | 79.2% |

| Sep-1994 | 79.6% |

| Oct-1994 | 79.6% |

| Nov-1994 | 79.8% |

| Dec-1994 | 79.8% |

| Jan-1995 | 79.7% |

| Feb-1995 | 80.0% |

| Mar-1995 | 79.9% |

| Apr-1995 | 79.8% |

| May-1995 | 79.7% |

| Jun-1995 | 79.5% |

| Jul-1995 | 79.7% |

| Aug-1995 | 79.6% |

| Sep-1995 | 79.8% |

| Oct-1995 | 79.8% |

| Nov-1995 | 79.7% |

| Dec-1995 | 79.7% |

| Jan-1996 | 79.8% |

| Feb-1996 | 79.9% |

| Mar-1996 | 79.9% |

| Apr-1996 | 79.9% |

| May-1996 | 80.0% |

| Jun-1996 | 80.1% |

| Jul-1996 | 80.4% |

| Aug-1996 | 80.5% |

| Sep-1996 | 80.4% |

| Oct-1996 | 80.6% |

| Nov-1996 | 80.5% |

| Dec-1996 | 80.5% |

| Jan-1997 | 80.5% |

| Feb-1997 | 80.4% |

| Mar-1997 | 80.6% |

| Apr-1997 | 80.7% |

| May-1997 | 80.6% |

| Jun-1997 | 80.9% |

| Jul-1997 | 81.1% |

| Aug-1997 | 81.3% |

| Sep-1997 | 81.1% |

| Oct-1997 | 81.1% |

| Nov-1997 | 81.0% |

| Dec-1997 | 81.0% |

| Jan-1998 | 81.0% |

| Feb-1998 | 81.0% |

| Mar-1998 | 81.0% |

| Apr-1998 | 81.1% |

| May-1998 | 81.0% |

| Jun-1998 | 81.0% |

| Jul-1998 | 81.1% |

| Aug-1998 | 81.2% |

| Sep-1998 | 81.3% |

| Oct-1998 | 81.1% |

| Nov-1998 | 81.2% |

| Dec-1998 | 81.3% |

| Jan-1999 | 81.8% |

| Feb-1999 | 81.5% |

| Mar-1999 | 81.3% |

| Apr-1999 | 81.3% |

| May-1999 | 81.4% |

| Jun-1999 | 81.4% |

| Jul-1999 | 81.2% |

| Aug-1999 | 81.3% |

| Sep-1999 | 81.3% |

| Oct-1999 | 81.5% |

| Nov-1999 | 81.6% |

| Dec-1999 | 81.5% |

| Jan-2000 | 81.8% |

| Feb-2000 | 81.8% |

| Mar-2000 | 81.7% |

| Apr-2000 | 81.9% |

| May-2000 | 81.5% |

| Jun-2000 | 81.5% |

| Jul-2000 | 81.3% |

| Aug-2000 | 81.1% |

| Sep-2000 | 81.1% |

| Oct-2000 | 81.1% |

| Nov-2000 | 81.3% |

| Dec-2000 | 81.4% |

| Jan-2001 | 81.4% |

| Feb-2001 | 81.3% |

| Mar-2001 | 81.3% |

| Apr-2001 | 80.9% |

| May-2001 | 80.8% |

| Jun-2001 | 80.6% |

| Jul-2001 | 80.5% |

| Aug-2001 | 80.2% |

| Sep-2001 | 80.2% |

| Oct-2001 | 79.9% |

| Nov-2001 | 79.7% |

| Dec-2001 | 79.8% |

| Jan-2002 | 79.6% |

| Feb-2002 | 79.8% |

| Mar-2002 | 79.6% |

| Apr-2002 | 79.5% |

| May-2002 | 79.4% |

| Jun-2002 | 79.2% |

| Jul-2002 | 79.1% |

| Aug-2002 | 79.3% |

| Sep-2002 | 79.4% |

| Oct-2002 | 79.2% |

| Nov-2002 | 78.8% |

| Dec-2002 | 79.0% |

| Jan-2003 | 78.9% |

| Feb-2003 | 78.9% |

| Mar-2003 | 79.0% |

| Apr-2003 | 79.1% |

| May-2003 | 78.9% |

| Jun-2003 | 78.9% |

| Jul-2003 | 78.8% |

| Aug-2003 | 78.7% |

| Sep-2003 | 78.6% |

| Oct-2003 | 78.6% |

| Nov-2003 | 78.7% |

| Dec-2003 | 78.8% |

| Jan-2004 | 78.9% |

| Feb-2004 | 78.8% |

| Mar-2004 | 78.7% |

| Apr-2004 | 78.9% |

| May-2004 | 79.0% |

| Jun-2004 | 79.1% |

| Jul-2004 | 79.2% |

| Aug-2004 | 79.0% |

| Sep-2004 | 79.0% |

| Oct-2004 | 79.0% |

| Nov-2004 | 79.1% |

| Dec-2004 | 78.9% |

| Jan-2005 | 79.2% |

| Feb-2005 | 79.2% |

| Mar-2005 | 79.2% |

| Apr-2005 | 79.4% |

| May-2005 | 79.5% |

| Jun-2005 | 79.2% |

| Jul-2005 | 79.4% |

| Aug-2005 | 79.6% |

| Sep-2005 | 79.4% |

| Oct-2005 | 79.3% |

| Nov-2005 | 79.2% |

| Dec-2005 | 79.3% |

| Jan-2006 | 79.6% |

| Feb-2006 | 79.7% |

| Mar-2006 | 79.8% |

| Apr-2006 | 79.6% |

| May-2006 | 79.7% |

| Jun-2006 | 79.8% |

| Jul-2006 | 79.8% |

| Aug-2006 | 79.8% |

| Sep-2006 | 79.9% |

| Oct-2006 | 80.1% |

| Nov-2006 | 80.0% |

| Dec-2006 | 80.1% |

| Jan-2007 | 80.3% |

| Feb-2007 | 80.1% |

| Mar-2007 | 80.2% |

| Apr-2007 | 80.0% |

| May-2007 | 80.0% |

| Jun-2007 | 79.9% |

| Jul-2007 | 79.8% |

| Aug-2007 | 79.8% |

| Sep-2007 | 79.7% |

| Oct-2007 | 79.6% |

| Nov-2007 | 79.7% |

| Dec-2007 | 79.7% |

| Jan-2008 | 80.0% |

| Feb-2008 | 79.9% |

| Mar-2008 | 79.8% |

| Apr-2008 | 79.6% |

| May-2008 | 79.5% |

| Jun-2008 | 79.4% |

| Jul-2008 | 79.2% |

| Aug-2008 | 78.8% |

| Sep-2008 | 78.8% |

| Oct-2008 | 78.4% |

| Nov-2008 | 78.1% |

| Dec-2008 | 77.6% |

| Jan-2009 | 77.0% |

| Feb-2009 | 76.7% |

| Mar-2009 | 76.2% |

| Apr-2009 | 76.2% |

| May-2009 | 75.9% |

| Jun-2009 | 75.9% |

| Jul-2009 | 75.8% |

| Aug-2009 | 75.6% |

| Sep-2009 | 75.1% |

| Oct-2009 | 75.0% |

| Nov-2009 | 75.2% |

| Dec-2009 | 74.8% |

| Jan-2010 | 75.1% |

| Feb-2010 | 75.1% |

| Mar-2010 | 75.1% |

| Apr-2010 | 75.4% |

| May-2010 | 75.1% |

| Jun-2010 | 75.2% |

| Jul-2010 | 75.1% |

| Aug-2010 | 75.0% |

| Sep-2010 | 75.1% |

| Oct-2010 | 75.0% |

| Nov-2010 | 74.8% |

| Dec-2010 | 75.0% |

| Jan-2011 | 75.2% |

| Feb-2011 | 75.1% |

| Mar-2011 | 75.3% |

| Apr-2011 | 75.1% |

| May-2011 | 75.2% |

| Jun-2011 | 75.0% |

| Jul-2011 | 75.0% |

| Aug-2011 | 75.1% |

| Sep-2011 | 74.9% |

| Oct-2011 | 74.9% |

| Nov-2011 | 75.3% |

| Dec-2011 | 75.4% |

| Jan-2012 | 75.5% |

| Feb-2012 | 75.5% |

| Mar-2012 | 75.7% |

| Apr-2012 | 75.7% |

| May-2012 | 75.7% |

| Jun-2012 | 75.6% |

| Jul-2012 | 75.6% |

| Aug-2012 | 75.7% |

| Sep-2012 | 76.0% |

| Oct-2012 | 76.1% |

| Nov-2012 | 75.8% |

| Dec-2012 | 76.0% |

| Jan-2013 | 75.6% |

| Feb-2013 | 75.8% |

| Mar-2013 | 75.8% |

| Apr-2013 | 75.8% |

| May-2013 | 76.0% |

| Jun-2013 | 75.9% |

| Jul-2013 | 76.0% |

| Aug-2013 | 76.0% |

| Sep-2013 | 76.0% |

| Oct-2013 | 75.6% |

| Nov-2013 | 76.1% |

| Dec-2013 | 76.1% |

| Jan-2014 | 76.4% |

| Feb-2014 | 76.4% |

| Mar-2014 | 76.5% |

| Apr-2014 | 76.5% |

| May-2014 | 76.4% |

| Jun-2014 | 76.9% |

| Jul-2014 | 76.7% |

| Aug-2014 | 76.9% |

| Sep-2014 | 76.8% |

| Oct-2014 | 76.9% |

| Nov-2014 | 76.9% |

| Dec-2014 | 77.1% |

| Jan-2015 | 77.1% |

| Feb-2015 | 77.2% |

| Mar-2015 | 77.1% |

| Apr-2015 | 77.2% |

| May-2015 | 77.2% |

| Jun-2015 | 77.4% |

| Jul-2015 | 77.1% |

| Aug-2015 | 77.3% |

| Sep-2015 | 77.2% |

| Oct-2015 | 77.2% |

| Nov-2015 | 77.4% |

| Dec-2015 | 77.4% |

| Jan-2016 | 77.7% |

| Feb-2016 | 77.8% |

| Mar-2016 | 77.9% |

| Apr-2016 | 77.8% |

| May-2016 | 77.9% |

| Jun-2016 | 77.9% |

| Jul-2016 | 78.0% |

| Aug-2016 | 77.9% |

| Sep-2016 | 78.0% |

| Oct-2016 | 78.1% |

| Nov-2016 | 78.1% |

| Dec-2016 | 78.1% |

| Jan-2017 | 78.2% |

| Feb-2017 | 78.3% |

| Mar-2017 | 78.5% |

| Apr-2017 | 78.6% |

| May-2017 | 78.5% |

| Jun-2017 | 78.6% |

| Jul-2017 | 78.8% |

| Aug-2017 | 78.4% |

| Sep-2017 | 79.0% |

| Oct-2017 | 78.7% |

| Nov-2017 | 78.9% |

| Dec-2017 | 79.0% |

| Jan-2018 | 78.9% |

| Feb-2018 | 79.3% |

| Mar-2018 | 79.2% |

| Apr-2018 | 79.2% |

| May-2018 | 79.3% |

| Jun-2018 | 79.4% |

| Jul-2018 | 79.6% |

| Aug-2018 | 79.3% |

| Sep-2018 | 79.4% |

| Oct-2018 | 79.6% |

| Nov-2018 | 79.6% |

| Dec-2018 | 79.5% |

| Jan-2019 | 79.8% |

| Feb-2019 | 79.9% |

| Mar-2019 | 79.8% |

| Apr-2019 | 79.7% |

| May-2019 | 79.7% |

| Jun-2019 | 79.7% |

| Jul-2019 | 79.6% |

| Aug-2019 | 80.0% |

| Sep-2019 | 80.2% |

| Oct-2019 | 80.3% |

| Nov-2019 | 80.3% |

| Dec-2019 | 80.4% |

| Jan-2020 | 80.6% |

| Feb-2020 | 80.5% |

| Mar-2020 | 79.5% |

| Apr-2020 | 69.6% |

| May-2020 | 71.4% |

| Jun-2020 | 73.5% |

| Jul-2020 | 73.8% |

| Aug-2020 | 75.2% |

| Sep-2020 | 75.1% |

| Oct-2020 | 76.1% |

| Nov-2020 | 76.0% |

| Dec-2020 | 76.3% |

| Jan-2021 | 76.4% |

| Feb-2021 | 76.6% |

| Mar-2021 | 76.8% |

| Apr-2021 | 76.9% |

| May-2021 | 77.1% |

| Jun-2021 | 77.2% |

| Jul-2021 | 77.8% |

| Aug-2021 | 77.9% |

| Sep-2021 | 78.0% |

| Oct-2021 | 78.4% |

| Nov-2021 | 78.9% |

| Dec-2021 | 79.2% |

| Jan-2022 | 79.2% |

| Feb-2022 | 79.5% |

| Mar-2022 | 80.0% |

| Apr-2022 | 79.9% |

| May-2022 | 80.0% |

| Jun-2022 | 79.8% |

| Jul-2022 | 79.9% |

| Aug-2022 | 80.2% |

| Sep-2022 | 80.2% |

| Oct-2022 | 79.9% |

| Nov-2022 | 79.8% |

| Dec-2022 | 80.1% |

| Jan-2023 | 80.3% |

| Feb-2023 | 80.5% |

| Mar-2023 | 80.7% |

| Apr-2023 | 80.7% |

| May-2023 | 80.7% |

| Jun-2023 | 80.9% |

| Jul-2023 | 80.9% |

| Aug-2023 | 80.8% |

| Sep-2023 | 80.8% |

| Oct-2023 | 80.6% |

| Nov-2023 | 80.7% |

| Dec-2023 | 80.4% |

| Jan-2024 | 80.6% |

| Feb-2024 | 80.7% |

| Mar-2024 | 80.7% |

| Apr-2024 | 80.8% |

| May-2024 | 80.8% |

| Jun-2024 | 80.8% |

| Jul-2024 | 80.9% |

| Aug-2024 | 80.9% |

| Sep-2024 | 80.9% |

| Oct-2024 | 80.6% |

| Nov-2024 | 80.4% |

Source: EPI analysis of Bureau of Labor Statistics’ Current Population Survey public data.

As the economy continued to improve, not only did unemployment fall precipitously, but the share of workers (re)entering the labor force continued to rise. As it turns out (and what we’ve long argued), workers have not been permanently sidelined from the Great Recession, but have systematically been returning to the labor market in search of opportunities. Over the last few years, the newly employed have been coming both from the ranks of the unemployed as well as from outside the labor force, those who were not actively seeking work the month prior to finding a job. In fact, the share of newly employed workers who did not look for work the previous month is at a historic high. Over 7-in-10 newly employed workers are coming from out of the labor force. Clearly, these sidelined workers wanted jobs, yet another indication that the unemployment rate is understating the extent of slack or job searchers compared to previous periods.

Share of newly employed workers who said that they were not actively searching for work in the previous month

| date | Share of newly employed workers who said that they were not actively searching for work in the previous month |

|---|---|

| Apr-1990 | 61.9% |

| May-1990 | 62.6% |

| Jun-1990 | 62.0% |

| Jul-1990 | 62.0% |

| Aug-1990 | 61.6% |

| Sep-1990 | 62.3% |

| Oct-1990 | 61.0% |

| Nov-1990 | 61.2% |

| Dec-1990 | 60.4% |

| Jan-1991 | 59.9% |

| Feb-1991 | 59.0% |

| Mar-1991 | 58.5% |

| Apr-1991 | 57.7% |

| May-1991 | 57.6% |

| Jun-1991 | 57.2% |

| Jul-1991 | 58.0% |

| Aug-1991 | 57.8% |

| Sep-1991 | 57.7% |

| Oct-1991 | 57.3% |

| Nov-1991 | 56.9% |

| Dec-1991 | 57.0% |

| Jan-1992 | 56.8% |

| Feb-1992 | 57.1% |

| Mar-1992 | 57.1% |

| Apr-1992 | 57.2% |

| May-1992 | 57.3% |

| Jun-1992 | 56.6% |

| Jul-1992 | 56.4% |

| Aug-1992 | 56.1% |

| Sep-1992 | 55.9% |

| Oct-1992 | 55.7% |

| Nov-1992 | 55.8% |

| Dec-1992 | 56.1% |

| Jan-1993 | 56.6% |

| Feb-1993 | 57.7% |

| Mar-1993 | 58.3% |

| Apr-1993 | 58.4% |

| May-1993 | 58.2% |

| Jun-1993 | 58.1% |

| Jul-1993 | 57.5% |

| Aug-1993 | 57.5% |

| Sep-1993 | 58.0% |

| Oct-1993 | 58.9% |

| Nov-1993 | 58.5% |

| Dec-1993 | 58.3% |

| Jan-1994 | 58.8% |

| Feb-1994 | 59.2% |

| Mar-1994 | 59.1% |

| Apr-1994 | 58.7% |

| May-1994 | 58.3% |

| Jun-1994 | 58.5% |

| Jul-1994 | 58.6% |

| Aug-1994 | 59.0% |

| Sep-1994 | 59.1% |

| Oct-1994 | 59.8% |

| Nov-1994 | 60.1% |

| Dec-1994 | 60.3% |

| Jan-1995 | 60.4% |

| Feb-1995 | 59.5% |

| Mar-1995 | 59.7% |

| Apr-1995 | 59.7% |

| May-1995 | 59.2% |

| Jun-1995 | 59.5% |

| Jul-1995 | 59.5% |

| Aug-1995 | 60.0% |

| Sep-1995 | 60.2% |

| Oct-1995 | 59.9% |

| Nov-1995 | 60.6% |

| Dec-1995 | 59.9% |

| Jan-1996 | 59.8% |

| Feb-1996 | 60.3% |

| Mar-1996 | 60.7% |

| Apr-1996 | 61.0% |

| May-1996 | 60.7% |

| Jun-1996 | 60.8% |

| Jul-1996 | 61.5% |

| Aug-1996 | 60.8% |

| Sep-1996 | 60.9% |

| Oct-1996 | 60.2% |

| Nov-1996 | 60.6% |

| Dec-1996 | 59.6% |

| Jan-1997 | 59.1% |

| Feb-1997 | 58.9% |

| Mar-1997 | 60.3% |

| Apr-1997 | 61.4% |

| May-1997 | 61.8% |

| Jun-1997 | 61.1% |

| Jul-1997 | 60.4% |

| Aug-1997 | 61.3% |

| Sep-1997 | 61.9% |

| Oct-1997 | 62.5% |

| Nov-1997 | 62.7% |

| Dec-1997 | 62.8% |

| Jan-1998 | 63.3% |

| Feb-1998 | 62.7% |

| Mar-1998 | 62.9% |

| Apr-1998 | 62.4% |

| May-1998 | 63.5% |

| Jun-1998 | 63.2% |

| Jul-1998 | 64.2% |

| Aug-1998 | 64.0% |

| Sep-1998 | 65.2% |

| Oct-1998 | 65.1% |

| Nov-1998 | 65.1% |

| Dec-1998 | 64.9% |

| Jan-1999 | 65.6% |

| Feb-1999 | 65.5% |

| Mar-1999 | 64.2% |

| Apr-1999 | 65.3% |

| May-1999 | 66.1% |

| Jun-1999 | 67.4% |

| Jul-1999 | 66.4% |

| Aug-1999 | 65.7% |

| Sep-1999 | 65.3% |

| Oct-1999 | 65.5% |

| Nov-1999 | 65.3% |

| Dec-1999 | 65.1% |

| Jan-2000 | 64.4% |

| Feb-2000 | 65.4% |

| Mar-2000 | 65.7% |

| Apr-2000 | 65.9% |

| May-2000 | 65.6% |

| Jun-2000 | 65.9% |

| Jul-2000 | 65.4% |

| Aug-2000 | 65.5% |

| Sep-2000 | 65.6% |

| Oct-2000 | 66.5% |

| Nov-2000 | 67.4% |

| Dec-2000 | 68.1% |

| Jan-2001 | 69.0% |

| Feb-2001 | 68.6% |

| Mar-2001 | 67.9% |

| Apr-2001 | 66.9% |

| May-2001 | 65.8% |

| Jun-2001 | 65.3% |

| Jul-2001 | 65.7% |

| Aug-2001 | 66.2% |

| Sep-2001 | 66.6% |

| Oct-2001 | 65.5% |

| Nov-2001 | 64.4% |

| Dec-2001 | 62.9% |

| Jan-2002 | 62.6% |

| Feb-2002 | 62.3% |

| Mar-2002 | 61.7% |

| Apr-2002 | 61.9% |

| May-2002 | 62.8% |

| Jun-2002 | 64.4% |

| Jul-2002 | 64.5% |

| Aug-2002 | 64.0% |

| Sep-2002 | 63.1% |

| Oct-2002 | 63.1% |

| Nov-2002 | 63.7% |

| Dec-2002 | 64.1% |

| Jan-2003 | 64.2% |

| Feb-2003 | 64.2% |

| Mar-2003 | 64.5% |

| Apr-2003 | 64.3% |

| May-2003 | 63.7% |

| Jun-2003 | 63.5% |

| Jul-2003 | 63.1% |

| Aug-2003 | 63.2% |

| Sep-2003 | 63.4% |

| Oct-2003 | 64.3% |

| Nov-2003 | 64.7% |

| Dec-2003 | 63.7% |

| Jan-2004 | 63.6% |

| Feb-2004 | 63.4% |

| Mar-2004 | 64.9% |

| Apr-2004 | 64.3% |

| May-2004 | 64.3% |

| Jun-2004 | 63.7% |

| Jul-2004 | 64.2% |

| Aug-2004 | 64.5% |

| Sep-2004 | 64.1% |

| Oct-2004 | 64.2% |

| Nov-2004 | 64.0% |

| Dec-2004 | 64.4% |

| Jan-2005 | 64.6% |

| Feb-2005 | 64.8% |

| Mar-2005 | 64.9% |

| Apr-2005 | 65.1% |

| May-2005 | 65.8% |

| Jun-2005 | 66.1% |

| Jul-2005 | 66.6% |

| Aug-2005 | 65.9% |

| Sep-2005 | 66.5% |

| Oct-2005 | 66.2% |

| Nov-2005 | 66.0% |

| Dec-2005 | 65.9% |

| Jan-2006 | 65.8% |

| Feb-2006 | 67.3% |

| Mar-2006 | 67.3% |

| Apr-2006 | 67.6% |

| May-2006 | 67.3% |

| Jun-2006 | 67.2% |

| Jul-2006 | 66.7% |

| Aug-2006 | 66.4% |

| Sep-2006 | 65.9% |

| Oct-2006 | 66.9% |

| Nov-2006 | 67.6% |

| Dec-2006 | 68.3% |

| Jan-2007 | 68.0% |

| Feb-2007 | 67.0% |

| Mar-2007 | 66.5% |

| Apr-2007 | 65.8% |

| May-2007 | 66.2% |

| Jun-2007 | 67.6% |

| Jul-2007 | 67.7% |

| Aug-2007 | 67.6% |

| Sep-2007 | 66.9% |

| Oct-2007 | 67.0% |

| Nov-2007 | 67.5% |

| Dec-2007 | 66.6% |

| Jan-2008 | 66.4% |

| Feb-2008 | 65.4% |

| Mar-2008 | 65.6% |

| Apr-2008 | 64.7% |

| May-2008 | 65.1% |

| Jun-2008 | 64.9% |

| Jul-2008 | 65.3% |

| Aug-2008 | 64.2% |

| Sep-2008 | 62.9% |

| Oct-2008 | 62.1% |

| Nov-2008 | 61.9% |

| Dec-2008 | 62.3% |

| Jan-2009 | 62.2% |

| Feb-2009 | 61.6% |

| Mar-2009 | 60.8% |

| Apr-2009 | 59.8% |

| May-2009 | 59.6% |

| Jun-2009 | 58.3% |

| Jul-2009 | 57.5% |

| Aug-2009 | 57.0% |

| Sep-2009 | 56.8% |

| Oct-2009 | 57.6% |

| Nov-2009 | 56.7% |

| Dec-2009 | 57.7% |

| Jan-2010 | 57.9% |

| Feb-2010 | 58.8% |

| Mar-2010 | 58.7% |

| Apr-2010 | 57.4% |

| May-2010 | 56.4% |

| Jun-2010 | 56.6% |

| Jul-2010 | 57.2% |

| Aug-2010 | 58.4% |

| Sep-2010 | 58.8% |

| Oct-2010 | 58.9% |

| Nov-2010 | 58.9% |

| Dec-2010 | 58.4% |

| Jan-2011 | 59.1% |

| Feb-2011 | 59.5% |

| Mar-2011 | 60.1% |

| Apr-2011 | 60.4% |

| May-2011 | 60.2% |

| Jun-2011 | 59.7% |

| Jul-2011 | 59.8% |

| Aug-2011 | 59.6% |

| Sep-2011 | 60.6% |

| Oct-2011 | 59.8% |

| Nov-2011 | 59.8% |

| Dec-2011 | 59.1% |

| Jan-2012 | 59.2% |

| Feb-2012 | 59.1% |

| Mar-2012 | 59.4% |

| Apr-2012 | 60.3% |

| May-2012 | 60.9% |

| Jun-2012 | 61.6% |

| Jul-2012 | 61.8% |

| Aug-2012 | 62.3% |

| Sep-2012 | 62.3% |

| Oct-2012 | 62.0% |

| Nov-2012 | 61.8% |

| Dec-2012 | 62.5% |

| Jan-2013 | 62.2% |

| Feb-2013 | 61.5% |

| Mar-2013 | 61.6% |

| Apr-2013 | 63.1% |

| May-2013 | 63.5% |

| Jun-2013 | 63.2% |

| Jul-2013 | 62.3% |

| Aug-2013 | 62.9% |

| Sep-2013 | 63.5% |

| Oct-2013 | 64.3% |

| Nov-2013 | 64.1% |

| Dec-2013 | 63.6% |

| Jan-2014 | 63.9% |

| Feb-2014 | 63.6% |

| Mar-2014 | 63.9% |

| Apr-2014 | 62.8% |

| May-2014 | 64.2% |

| Jun-2014 | 64.5% |

| Jul-2014 | 66.0% |

| Aug-2014 | 65.5% |

| Sep-2014 | 65.3% |

| Oct-2014 | 64.9% |

| Nov-2014 | 65.3% |

| Dec-2014 | 65.8% |

| Jan-2015 | 67.2% |

| Feb-2015 | 67.8% |

| Mar-2015 | 68.5% |

| Apr-2015 | 68.1% |

| May-2015 | 68.5% |

| Jun-2015 | 68.1% |

| Jul-2015 | 68.9% |

| Aug-2015 | 68.6% |

| Sep-2015 | 68.8% |

| Oct-2015 | 68.7% |

| Nov-2015 | 68.5% |

| Dec-2015 | 69.0% |

| Jan-2016 | 68.7% |

| Feb-2016 | 70.2% |

| Mar-2016 | 71.2% |

| Apr-2016 | 71.2% |

| May-2016 | 69.5% |

| Jun-2016 | 68.6% |

| Jul-2016 | 68.6% |

| Aug-2016 | 69.5% |

| Sep-2016 | 69.1% |

| Oct-2016 | 67.9% |

| Nov-2016 | 67.4% |

| Dec-2016 | 68.6% |

| Jan-2017 | 69.5% |

| Feb-2017 | 69.5% |

| Mar-2017 | 69.6% |

| Apr-2017 | 70.0% |

| May-2017 | 70.2% |

| Jun-2017 | 70.5% |

| Jul-2017 | 70.1% |

| Aug-2017 | 70.7% |

| Sep-2017 | 70.3% |

| Oct-2017 | 70.2% |

| Nov-2017 | 70.2% |

| Dec-2017 | 70.2% |

| Jan-2018 | 71.2% |

| Feb-2018 | 71.4% |

| Mar-2018 | 71.5% |

| Apr-2018 | 71.5% |

| May-2018 | 71.5% |

| Jun-2018 | 72.3% |

| Jul-2018 | 72.8% |

| Aug-2018 | 72.8% |

| Sep-2018 | 72.8% |

| Oct-2018 | 72.4% |

| Nov-2018 | 72.6% |

| Dec-2018 | 72.5% |

| Jan-2019 | 72.4% |

| Feb-2019 | 72.5% |

| Mar-2019 | 72.0% |

| Apr-2019 | 72.4% |

| May-2019 | 73.1% |

| Jun-2019 | 73.8% |

| Jul-2019 | 74.2% |

| Aug-2019 | 73.7% |

| Sep-2019 | 73.6% |

| Oct-2019 | 74.1% |

| Nov-2019 | 74.4% |

| Dec-2019 | 74.2% |

| Jan-2020 | 73.1% |

| Feb-2020 | 72.6% |

| Mar-2020 | 73.0% |

| Apr-2020 | 73.0% |

| May-2020 | 62.3% |

| Jun-2020 | 50.2% |

| Jul-2020 | 41.2% |

| Aug-2020 | 44.3% |

| Sep-2020 | 50.2% |

| Oct-2020 | 54.4% |

| Nov-2020 | 58.3% |

| Dec-2020 | 61.6% |

| Jan-2021 | 62.7% |

| Feb-2021 | 63.1% |

| Mar-2021 | 63.5% |

| Apr-2021 | 65.3% |

| May-2021 | 66.5% |

| Jun-2021 | 67.1% |

| Jul-2021 | 67.5% |

| Aug-2021 | 67.8% |

| Sep-2021 | 68.3% |

| Oct-2021 | 69.1% |

| Nov-2021 | 70.1% |

| Dec-2021 | 70.4% |

| Jan-2022 | 71.0% |

| Feb-2022 | 70.7% |

| Mar-2022 | 71.1% |

| Apr-2022 | 71.7% |

| May-2022 | 72.8% |

| Jun-2022 | 73.1% |

| Jul-2022 | 72.5% |

| Aug-2022 | 72.3% |

| Sep-2022 | 72.7% |

| Oct-2022 | 73.7% |

| Nov-2022 | 73.5% |

| Dec-2022 | 73.6% |

| Jan-2023 | 73.9% |

| Feb-2023 | 74.9% |

| Mar-2023 | 74.9% |

| Apr-2023 | 74.4% |

| May-2023 | 74.4% |

| Jun-2023 | 74.6% |

| Jul-2023 | 73.9% |

| Aug-2023 | 73.9% |

| Sep-2023 | 72.9% |

| Oct-2023 | 72.8% |

| Nov-2023 | 71.6% |

| Dec-2023 | 70.9% |

| Jan-2024 | 71.6% |

| Feb-2024 | 72.5% |

| Mar-2024 | 73.8% |

| Apr-2024 | 72.9% |

| May-2024 | 71.8% |

| Jun-2024 | 71.3% |

| Jul-2024 | 71.4% |

| Aug-2024 | 71.0% |

| Sept-2024 | 69.7% |

| Oct-2024 | 69.5% |

| Nov-2024 | 70.8% |

Note: Bureau of Labor Statistics, Labor Force Flows: Unemployed to Employed (16 Years and Over) [LNS17100000], and Not in Labor Force to Employed (16 years and over) [LNS17200000]. Because of volatility in these data, the line reflects a three month moving averages.

Source: EPI analysis of Bureau of Labor Statistics Current Population Survey public data series.

By banning mandatory arbitration clauses and class and collective action waivers, Congress could restore a fundamental workers right

Last term, the Supreme Court dealt a significant blow to the fundamental right of workers in this country to join together to address workplace disputes. In Epic Systems v. Lewis, the Court, by a 5-4 majority, held that an employer may lawfully require its employees to agree, as a condition of employment, to resolve all workplace disputes on an individual basis in arbitration. Siding with employers and the Trump administration, the Court’s decision paves the way for the majority of workers in this country to be forced to sign away their right to pursue workplace disputes on a collective or class basis. Available data suggests that, unless Congress acts, more than 80 percent of workplaces will subject their workers to mandatory arbitration with class and collective action waivers within six years.

Mandatory arbitration clauses rob workers of their right to take their employer to court for all types of employment-related claims, forcing workers into a process that overwhelmingly favors employers. Class and collective action waivers go one step further, forcing workers to manage this process alone, even though these issues are rarely confined to one single worker.

Workers depend on collective and class actions to enforce many workplace rights. Employment class actions have helped to combat race and sex discrimination and are fundamental to the enforcement of wage and hour standards. Without the ability to aggregate claims, it is very difficult, if not impossible, for workers to find legal representation in these matters. This is particularly true for low-wage workers, whose cases are unlikely to involve large enough awards to attract attorneys to invest time in the case. Class and collective action suits allow workers to pool their claims, making it possible for an attorney to earn enough to make the case worth pursuing.

The new Democratic House should make worker empowerment a priority

For the first time in nearly a decade, Democrats will hold the majority in the House when Congress convenes in January. The results of yesterday’s election are encouraging and represent historic progress—with a record number of women winning seats in the house, including key victories by diverse candidates across faiths and ethnicities. And importantly, Democrats won the popular vote in the House by a 9.2 percent margin despite today’s 3.7 percent unemployment rate, which should have provide great advantage to the incumbent party.

It is nevertheless important to note that with Republicans in control of the Senate and the White House, it is unlikely that policies that promote a just economy for working people will become law. Still, House Democrats have the opportunity to advance long overdue reforms. It is critical that they focus on an agenda that serves our nation’s workers. This must include House Democrats working to raise workers’ wages, restore workers’ access to justice on the job, and promote workers’ right to collectively bargain.

Workers deserve a fair minimum wage. At $7.25 per hour, the federal minimum wage is now more than 25 percent below where it was in real terms half a century ago. House Democrats must advance legislation to raise the federal minimum wage to $15 per hour by 2024, indexing it to the national median wage thereafter, and phasing out the tipped minimum wage and other subminimum wages. Given inflation expectations, $15 in 2024 would be around $13.00 in 2018 dollars, an appropriate level for the federal floor. The Raise the Wage Act introduced this Congress included all of these reforms. The House must work to pass similar legislation in the new Congress.

Workers should not be forced to sign away their rights as a condition of employment. The use of mandatory arbitration and collective and class action waivers—under which workers are forced to handle workplace disputes as individuals through arbitration, rather than being able to resolve these matters together in court—makes it more difficult for workers to enforce their rights. These agreements bar access to the courts for all types of employment-related claims, including those based on the Fair Labor Standards Act, Title VII of the Civil Rights Act, and the Family Medical Leave Act. This means that a worker who is not paid fairly, discriminated against, or sexually harassed, is forced into a process that overwhelmingly favors the employer—and forced to manage this process alone, even though these issues are rarely confined to one single worker. Congress must act to ban mandatory arbitration agreements and class and collective action waivers. The Restoring Justice for Workers Act introduced this Congress includes all of these reforms. The House should work to pass this important reform in the new Congress.

Voters in Missouri and Arkansas just lifted pay for 1 million workers

In yesterday’s election, voters in Missouri and Arkansas gave overwhelming approval to ballot measures that will raise their state’s minimum wage over the next several years, lifting pay for a combined 1 million workers. In Missouri, 62 percent of voters elected to raise the state minimum wage from its current $7.85 to $12 an hour in 2023. In Arkansas, 68 percent of voters supported a measure that will raise the state minimum wage to $11 per hour in 2021 from its current value of $8.50.

The increase in Arkansas will raise pay for an estimated 300,000 workers (about a quarter of the state’s wage-earning workforce). The Missouri increase will lift pay for 677,000 workers (also about a quarter of wage-earners in the state.) In both cases, the majority of workers who will get a raise are women, most work full time, and they come from families with modest incomes. Analyses of the measures estimate that the raise in Arkansas will put over $400 million into the pockets of low-wage workers there over the course of the increases. In Missouri, low-wage workers will receive nearly $870 million in additional wages over the course of the measure’s implementation.

In voting to raise their state minimum wages, voters in Arkansas and Missouri are making long-overdue corrections to policy failures that political leaders in those states, and at the federal level, should have fixed a long time ago. Raising the minimum wage in Arkansas to $11 by 2021 and $12 by 2023 in Missouri will bring the minimum wage in those states, in both cases, roughly back to where the federal minimum wage was in 1968, when it equaled roughly $10 an hour in today’s dollars. According to the Congressional Budget Office’s (CBO’s) projections for inflation, $11 in 2021 is $9.98 in 2017 dollars, $12 in 2023 is $10.40 in 2017 dollars.

Updating key labor standards, like the minimum wage, is critical if policymakers want to do something about the enormous stagnation in wages that has plagued the country for decades. The recent modest uptick in wage growth is not nearly enough to undo the damage that has been done over the past 70 years. Since the mid-1970s, as the U.S. economy has grown and productivity has risen, hourly pay has barely budged after adjusting for inflation. Since 1973, average labor productivity has grown 77 percent; yet hourly compensation for the typical U.S. worker—and this includes both wages and benefits, such as payments for healthcare premiums and retirement accounts—has grown only 12.4 percent. For low-wage workers, the trends are even worse.

Heading into the midterms, there’s still no evidence that the TCJA is working as promised

It’s been widely reported that going into this year’s elections, Republicans aren’t running on their signature tax law from last year—the Tax Cuts and Jobs Act (TCJA). It’s not difficult to see why. The TCJA is increasingly unpopular, and a recent GOP internal poll shows that respondents say the law benefits “large corporations and rich Americans” over “middle class families.”

Republicans shouldn’t find this so surprising—since the law they wrote was a massive giveaway to the rich and big corporations. And voters do not appear fooled by a PR campaign earlier this year where corporate allies tried to trick workers into believing that any bonus they received in 2017 was due to the TCJA.

The claims of immediate benefits to workers by those corporate allies should never have been taken so seriously by the media. The theory justifying claims that corporate rate cuts should trickle down to typical workers always required that a long chain of economic events to occur first. We’ve long pointed out that nearly every single link in this chain is likely to break down. The first link in this chain concerns firms’ investment; anyone trying to discern if the corporate rate cuts are having their promised effects for workers should be watching investment like a hawk.

The story here doesn’t look any better for proponents of the TCJA than it did in September. The quarterly growth rate in business investment cratered in the third quarter of the year, growing at a 0.8 percent annualized rate. The administration’s favorite data point, the year-over-year increase in real, private nonresidential fixed investment, slowed from 7.1 percent in the 2nd quarter of 2018 to 6.4 percent in the 3rd quarter. Charted below, the data still doesn’t show the clear boost to the trend of investment that would indicate a positive effect coming from the TCJA.

No evidence that the TCJA has increased investment: Year-over-year change in real, nonresidential fixed investment, 2003Q1-2018Q3

| date | NRFI |

|---|---|

| 2003Q1 | -2.3% |

| 2003Q2 | 1.6% |

| 2003Q3 | 4.0% |

| 2003Q4 | 6.8% |

| 2004Q1 | 5.2% |

| 2004Q2 | 4.9% |

| 2004Q3 | 5.7% |

| 2004Q4 | 6.5% |

| 2005Q1 | 9.2% |

| 2005Q2 | 8.2% |

| 2005Q3 | 7.4% |

| 2005Q4 | 6.1% |

| 2006Q1 | 8.0% |

| 2006Q2 | 8.2% |

| 2006Q3 | 7.8% |

| 2006Q4 | 8.1% |

| 2007Q1 | 6.5% |

| 2007Q2 | 7.0% |

| 2007Q3 | 6.8% |

| 2007Q4 | 7.3% |

| 2008Q1 | 5.8% |

| 2008Q2 | 3.8% |

| 2008Q3 | 0.2% |

| 2008Q4 | -7.0% |

| 2009Q1 | -14.4% |

| 2009Q2 | -17.1% |

| 2009Q3 | -16.1% |

| 2009Q4 | -10.3% |

| 2010Q1 | -2.3% |

| 2010Q2 | 4.1% |

| 2010Q3 | 7.5% |

| 2010Q4 | 8.9% |

| 2011Q1 | 8.0% |

| 2011Q2 | 7.3% |

| 2011Q3 | 9.3% |

| 2011Q4 | 10.0% |

| 2012Q1 | 12.9% |

| 2012Q2 | 12.6% |

| 2012Q3 | 7.2% |

| 2012Q4 | 5.6% |

| 2013Q1 | 4.3% |

| 2013Q2 | 2.3% |

| 2013Q3 | 4.4% |

| 2013Q4 | 5.4% |

| 2014Q1 | 5.4% |

| 2014Q2 | 7.6% |

| 2014Q3 | 8.0% |

| 2014Q4 | 6.4% |

| 2015Q1 | 4.5% |

| 2015Q2 | 2.7% |

| 2015Q3 | 0.8% |

| 2015Q4 | -0.7% |

| 2016Q1 | -0.5% |

| 2016Q2 | -0.1% |

| 2016Q3 | 0.8% |

| 2016Q4 | 1.8% |

| 2017Q1 | 4.4% |

| 2017Q2 | 5.3% |

| 2017Q3 | 5.0% |

| 2017Q4 | 6.3% |

| 2018Q1 | 6.7% |

| 2018Q2 | 7.1% |

| 2018Q3 | 6.4% |

Source: EPI analysis of data from table 1.1.6 from the National Income and Product Accounts (NIPA) from the Bureau of Economic Analysis (BEA).

Latina workers have to work 10 months into 2018 to be paid the same as white non-Hispanic men in 2017

November 1 is Latina Equal Pay Day, the day that marks how long into 2018 a Latina would have to work in order to be paid the same wages her white male counterpart was paid last year. That’s just over 10 months longer, meaning that Latina workers had to work all of 2017 and then this far—to November 1!—into 2018 to get paid the same as white non-Hispanic men did in 2017. Put another way, a Latina would have to be in the workforce for 55 years to earn what a non-Hispanic white man would earn after 30 years in the workforce. Unfortunately, Hispanic women are subject to a double pay gap—an ethnic pay gap and a gender pay gap.

The date November 1 is based on the finding that Hispanic women workers are paid 54 cents on the white non-Hispanic male dollar, using the 2016 March Current Population Survey for median annual earnings for full-time, year-round workers. We get similar results when we look at hourly wages for all workers (not just full-time workers) using the monthly Current Population Survey Outgoing Rotation Group for 2017—which show Hispanic women workers being paid 58 cents on the white male dollar.

This gap narrows—but not dramatically—when we control for education, years of experience, and location by regression-adjusting the differences between workers. Using this method, we find that, on average, Latina workers are paid only 66 cents on the dollar relative to white non-Hispanic men.

Yet another reason why Megyn Kelly does not need your sympathy

Megyn Kelly is out at NBC after an uproar over her comments in defense of blackface Halloween costumes during an episode of her television show last week. NBC has canceled “Megyn Kelly Today” and Kelly will be negotiating an exit from her contract. Speculation that Kelly would get a full payout for her three-year, $69 million contract drew a bitter response from people on Twitter. “Congrats to Megyn Kelly for getting $69 million for thinking blackface is fine,” one person tweeted.

Kelly’s unfathomable severance package isn’t the only thing separating her from regular working people. She actually may have a say in her noncompete clause. According to The Hollywood Reporter, her legal representation is “attempting to keep her noncompete clause as short as possible. Six months is the standard in the television news industry.”

Nearly one in five U.S. workers are bound by noncompete agreements, which block them from working for a competitor for a set period of time if they leave their current job. That’s nearly 30 million people who have essentially lost their full right to leave their jobs. And it’s not just highly paid workers who are required to sign them—14.3 percent of workers without a four-year college degree and 13.5 percent of workers earning up to $40,000 a year have noncompetes.

Noncompetes are a big problem. If you are a typical worker and you are not in a union, one of the most important points of leverage you have to negotiate for a raise or fight back against abuse is the fact that you can quit and work somewhere else. A noncompete agreement weakens your power: you have to stay with your employer because you can’t seek or accept a better-paying job with a competitor.

The “boom” of 2018 tells us that fiscal stimulus works, but that the GOP has only used it when it helps their reelection, not when it helps typical families

The Commerce Department released data today on the growth in gross domestic product (GDP—the widest measure of economic activity) in the 3rd quarter of 2018. It showed growth at a 3.5 percent rate in this quarter, down slightly from 4.2 percent growth in the second quarter of 2018. For comparison, in the run-up to the 2016 presidential elections, economic growth had barely averaged 2 percent since recovery from the Great Recession began in mid-2009.

White House economic adviser Larry Kudlow refers to this recent pick-up in growth as the “boom” of 2018. While Kudlow is always hyperbolic and almost always wrong, especially about “booms” (he pronounced in December 2007—the last month before the Great Recession—that “there’s no recession coming. The pessimistas were wrong. It’s not going to happen…. The Bush boom is alive and well.”), it remains worth asking: what is the basis of the faster growth so far in in 2018?

The answer is simple: a pronounced swing from fiscal austerity to fiscal stimulus, enacted by a Republican Congress that decided to help, rather than hurt, the economic recovery once it was being helmed by a Republican president. Yes, that sounds like a harsh and partisan judgement, but it’s the only rational reading of recent years’ evidence.

In the run-up to the 2016 elections, we documented clearly that that recovery from the Great Recession had been intentionally throttled by a historically large dose of austerity; specifically, historically slow growth in public spending. The main actors in imposing that austerity were Republicans in Congress, with some assists from Republican governors and state legislatures (think Sam Brownback from Kansas and Scott Walker from Wisconsin). The quick federal pivot to stimulus once the White House changed hands in 2017 makes the political roots of all this pretty clear.

Six reasons not to put too much weight on the new study of Seattle’s minimum wage

Seattle’s minimum wage increases are one of the most important local policy developments in recent years, but the new study by University of Washington researchers Jardim et al. (2018) is largely uninformative about the effects of the policy because it uses the same flawed methodology that economists criticized in connection with earlier studies by the group. But, even if you believe the results of the new study, a careful reading of its actual findings shows the minimum wage benefited all of the city’s low-wage workers who had jobs prior to the increase.

1. The new study is based on a flawed comparison between Seattle and other areas in Washington state. The comparison causes the study to measure a reduction in the number of new jobs under $15/hour, when in fact this is not a cause for concern.

By comparing workers in Seattle with workers elsewhere in Washington state, the study incorrectly assumes that the low-wage labor market in Seattle would have grown like other areas in Washington, were it not for the city’s 2015-2016 minimum wage increases. This comparison is unreasonable because, as other researchers have demonstrated (Dube 2017, Rothstein and Schanzenbach 2017, Zipperer and Schmitt 2017), Seattle experienced much faster wage gains for reasons that had nothing to do with the minimum wage. Indeed, the authors of the new study find that Seattle had faster wage growth and diverged from other regions prior to the city’s minimum wage increases (see their Table 8 for the 2012-2013 period).

The flawed comparison underlying the study causes it to mistakenly attribute negative employment changes to the minimum wage, when in reality Seattle’s economic boom simply meant that low-wage jobs were converted into higher-wage jobs. For example, the authors document a decline in newly employed workers earning less than $15/hour and argue that the minimum wage is causing “losses in employment opportunities.” Instead, as jobs in Seattle’s tightening labor market were upgraded from lower-wage to higher-wage jobs, there was a mechanical decline in the number of new entrants under any given low-wage threshold. The purported decline in new entrants is not a cause for concern. The fast wage growth in Seattle relative to comparison regions prevents the study from making credible claims about the consequences of the city’s minimum wage increases in 2015 and 2016.

Top 1.0 percent reaches highest wages ever—up 157 percent since 1979

Newly available wage data for 2017 show that annual wages grew far faster for the top 1.0 percent (3.7 percent) than for the bottom 90 percent (up only 1.0 percent). The top 0.1 percent saw the fastest growth, up 8.0 percent—far faster than any other wage group. This fast wage growth for the top 0.1 percent reflects the sharp 17.6 percent spike upwards in the compensation of the CEOs of large firms: executives comprise the largest group in both the top 1.0 and top 0.1 percent of earners. The fast wage growth of the top 1.0 percent in 2017 brought their wages to the highest level ever, $719,000, topping the wage levels reached before the Great Recession of $716,000 in 2007. The wages of the top 0.1 percent reached $2,757,000 in 2017, the second highest level ever, roughly only 4 percent below their wages in 2007.

These are the results of EPI’s updated series on wages by earning group, which is developed from published Social Security Administration data. These data, unlike the usual source of our wage analyses (the Current Population Survey) allow us to estimate wage trends for the top 1.0 and top 0.1 percent of earners, as well as those for the bottom 90 percent and other categories among the top 10 percent of earners. These data are not topcoded, meaning the underlying earnings reported are actual earnings and not “capped” for confidentiality.

What to Watch on Jobs Day: Keeping an eye on the teacher jobs gap

On Friday, the Bureau of Labor Statistics will release September’s numbers on the state of the labor market. As usual, I’ll be paying close attention to nominal wage growth as well as the prime-age employment-to-population ratio, which are two of the best indicators of labor market health. Friday’s report will also give us a chance to examine the “teacher gap”—the gap between local public education employment and what is needed to keep up with growth in the student population.

Thousands of local public education jobs were lost during the recession, and those losses continued deep into the official economic recovery, even as more students started school each year. This has been true of public sector jobs in general—continued austerity at all levels of government has been a drag on public sector employment, which has failed to keep up with population growth.

Teacher strikes in several states over the last couple of years have highlighted deteriorating teacher pay as a critical issue. My colleague Emma Garcia has forthcoming work that further documents shortcomings in the teaching profession today, including important issues of quality, particularly worse in high-poverty schools.

The costs of a significant teacher gap are high, and consequences measurable: larger class sizes, fewer teacher aides, fewer extracurricular activities, and changes to curricula. Last year, the local public education job shortfall remained large. To solve this problem, state and local governments need to fund more teaching positions and raise pay to close the teacher pay gap and attract and retain high quality teachers. On Friday, I will compare where jobs in public education should be, using the pre-recession ratio, student population growth, and the most recent jobs numbers.

The Fed’s current path might be leaving lots of money on the table unnecessarily

Today the Federal Reserve Open Market Committee (FOMC) will almost surely announce it is continuing on its path of steady interest rate hikes. These hikes are meant to start slowing the growth of the U.S. economy in the name of getting ahead of the curve on any potential outbreak of inflation. It’s important to be really clear on this point. The Fed is trying to keep economic growth slower than it would have otherwise been, and unemployment higher than it would otherwise have been, if they had not raised rates.

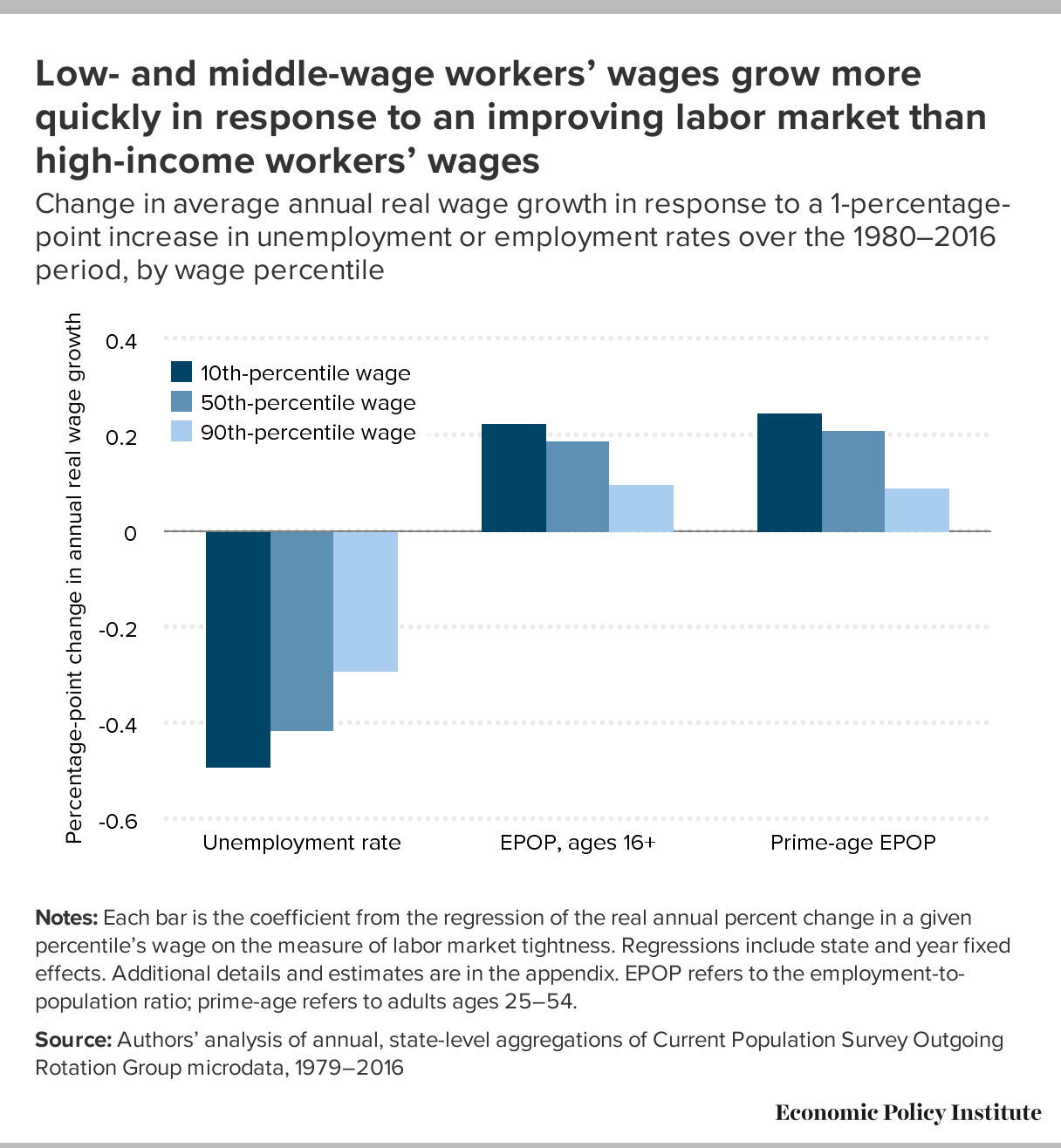

Intentionally keeping unemployment higher than it would have been will strike many as hard to believe—why would the Fed ever do this? The reason is that they see their job as balancing the obvious (but still underappreciated) benefits of low unemployment against the risk that unemployment will get so low that workers are empowered to achieve wage increases so large that they threaten to push up inflation. They’re not wrong that falling unemployment would eventually lead to faster wage growth. A primary way that workers (especially nonunionized workers) get raises is by either leaving their current job for a better one, or threatening to leave if their bosses don’t give them a raise. When unemployment is higher, fewer better-paying jobs are out there for workers to move to, and bosses know this and don’t find threats to leave all that credible. This intuition is confirmed by data—lower unemployment is clearly associated with faster wage growth, and this effect is most pronounced for low- and moderate-wage workers with few other sources of leverage in the labor market to get raises.

{kind=link}

Defenders of the Fed’s current path would say that it makes sense when judged by the past history of the Fed—unemployment today sits below 4 percent, well below conventional estimates of the “natural” rate of unemployment that is meant to define the lowest sustainable rate of non-inflationary unemployment.

Exploring the effects of student absenteeism

With the great majority of states choosing some measurement of school attendance as their so-called “fifth metric” required by the Every School Succeeds Act,1 researchers, policymakers, and advocates are questioning how useful these metrics are at informing us about student achievement and education equity, as well as guiding policy. Indeed, while research has linked missing school to elevated risk of dropping out and poorer graduation rates, policymakers and researchers should further explore the importance of missing school, and about factors driving student absenteeism, and how to reduce it.

Our recently released report, Student absenteeism:Who misses school and how missing school matters for performance, examines how much school students are missing, which groups of students are missing the most school, and how bad missing school is for performance. We learned that about one in five students—19.2 percent—missed three or more days of school in the month before they took the 2015 National Assessment of Educational Progress (NAEP) assessment. Students who have been diagnosed with a disability, Hispanic-English language learners, Native Americans, and students who are eligible for free lunch, were the most likely to miss school, while Asian students were rarely absent. Our findings also confirmed that missing school negatively effects performance, even after accounting for student and school characteristics (including gender, race/ethnicity, language status, disability status, income, and school socioeconomic characteristics). Even students with only occasional absences were negatively affected. For these students, relative to those who did not miss school, absenteeism makes a moderate dent in their performance (a tenth of a standard deviation), but the decline in performance becomes more troubling as the number of missed days increases (up to about two-thirds of a standard deviation for those missing more than 10 school days).

Data continues to show little evidence that tax cuts are trickling down to typical workers, and now House Republicans want a do-over

In December, when Republicans passed the Tax Cuts and Jobs Act (TCJA) they chose to make tax cuts for corporations permanent, while making the individual provisions temporary to satisfy the requirements of budget reconciliation. Republicans sold these corporate tax cuts as being beneficial to everyday working people, despite the fact that previous experience gives us no reason to believe that corporate rate cuts will trickle down to anyone.

Some willing allies in the corporate world, eager to bolster the case for tax cuts, tried to hoodwink workers into believing that any bonus a worker received in 2017 was due to the TCJA. But the economic theory behind the idea that corporate rate cuts lead to higher pay for typical workers does not say that those wage increases would occur immediately (and certainly not before the tax cuts came into effect). Instead, wage bumps for workers, if they come at all, would come only after a long chain of economic events were triggered by the cut. One of the first of these events should be increased investment. We’ve long pointed out that there was reason to believe that nearly every link in this chain would break down, and that the theory itself is inconsistent with the reality of the larger deficits caused by the TCJA.

Now that the tax cuts have passed and enough time has gone by to allow some data to trickle in, is there any reason for us to change this judgement? Not really. There’s still no indication in the data that the TCJA has spurred investment—the necessary but by no means sufficient precursor to wage gains. Sure, owners of corporate shares have made out like bandits. The most recent release from the Bureau of Economic Analysis (BEA) shows that domestic after-tax corporate profits remain high, 7.5 percent of GDP in the second quarter of 2018 compared to 7.4 percent in the first quarter of 2018 and up substantially from already-high levels (6.7 percent) in 2017. Revenue collected from domestic corporate taxes remains low, 1.2 percent of GDP in the second quarter of 2018 compared to 1.1 percent in the first quarter of 2018 and 1.8 percent in 2017. Finally, undistributed domestic corporate profits – corporate profits kept internal to the firm and not distributed back to shareholders as dividends—remain historically high. This is due to the windfall the TCJA contained for multinational corporations on the profits they booked offshore. These undistributed profits (available to finance share buybacks) constituted 8.9 percent of domestic corporate gross value added in the second quarter of 2018 compared to 13.7 percent in the first quarter of 2018 and 2.6 percent in 2017. In short, the direct effects of the TCJA are here and totally visible in the data: swollen corporate profits.

Further evidence that the tax cuts have not led to widespread bonuses, wage or compensation growth

One of the leading arguments for the GOP’s Tax Cuts and Jobs Act of 2017 has been that it will raise the wages of rank-and-file workers, with congressional Republicans and members of the Trump administration promising raises of many thousands of dollars within ten years. The Trump administration’s chair of the Council of Economic Advisers argued in April that we are already seeing the positive wage impact of the tax cuts: