Fed should hold steady—the economy had “room to run” over past year and may well have more in the next year

The Fed’s Federal Open Market Committee (FOMC) will debate again this week whether or not they should raise interest rates to slow the economic recovery in an effort to forestall potential inflation.

The debate over when the Federal Reserve should begin raising its short-term policy interest really began in earnest in September 2015. In the month before the FOMC met in September 2015, futures markets put the odds of a rate hike at over 50 percent. It is likely that all that kept the hike from happening in September of that year was the surprise financial market declines in China, which spilled over into the American stock exchanges for a spell. In December 2015, after this short-term drama passed, the Fed raised rates for the first time in seven years.

In the debate that accompanied the run-up to the September 2015 meeting, those arguing for further patience from the Fed (like this author) argued that there remained lots of slack remaining in the labor market, and that this slack would contain inflationary pressures. One source of slack identified was a potential firming-up of labor force participation, which had dropped considerably over the recovery.

In retrospect, this seems clearly correct. Since September 2015, the headline unemployment rate has been essentially flat. The Congressional Budget Office (CBO) projects that the 2016-2020 trend in potential labor force growth is 0.4-0.5 percent. If employment growth just grew at trend after September 2015, there would have been roughly 700,000 jobs created between September 2015 and 2016. In reality, just under 2.5 million jobs were created, meaning that employment was growing much faster than trend.

Where did all of these extra, “above-trend”workers come from? Largely from a firming-up of the labor force participation rate, which rose from 62.4 to 62.9 in the year after September 2015. This translates into about 1.3 additional workers.

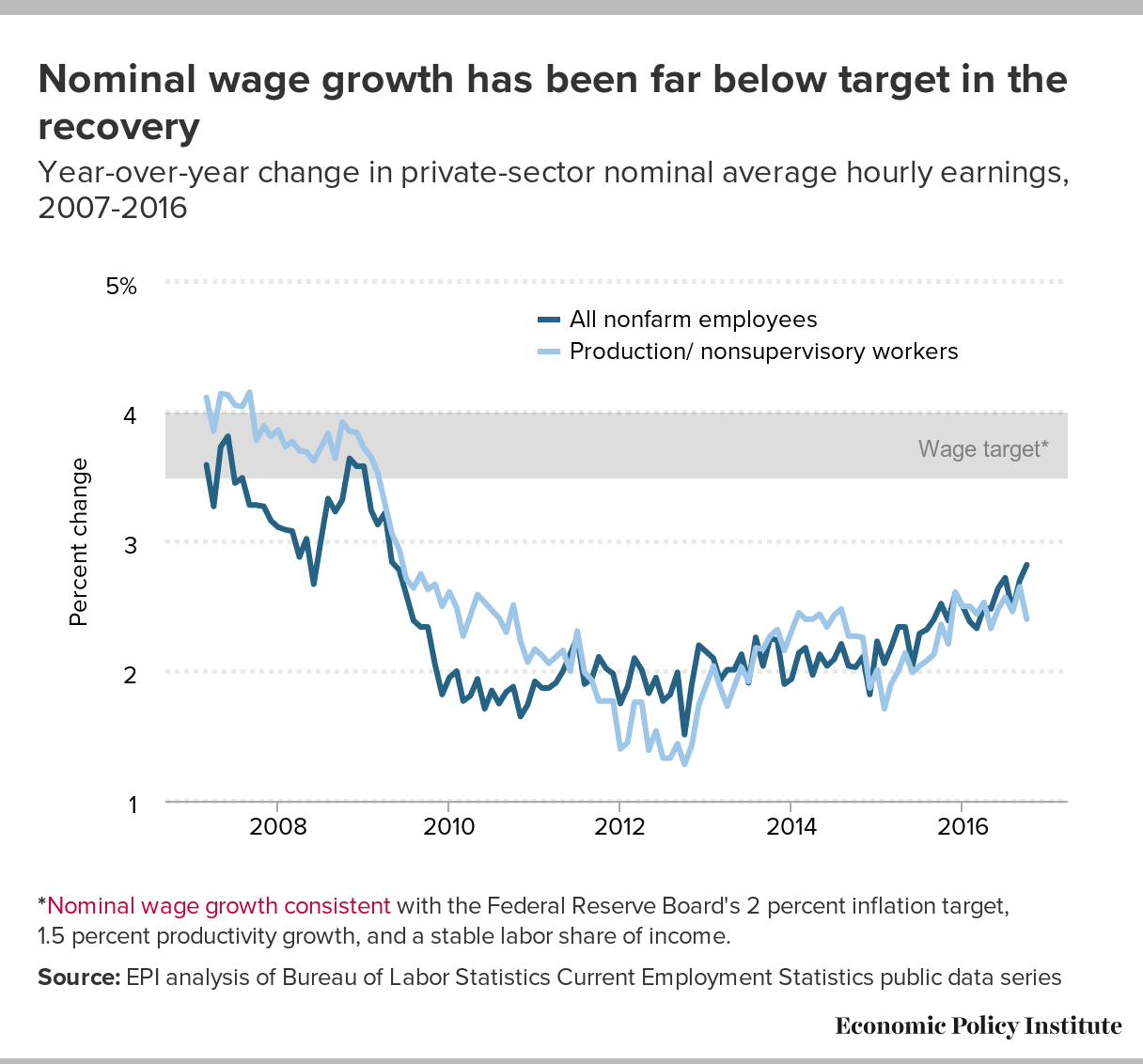

Absorbing potential workers who had abandoned active search (and hence were no longer classified as officially unemployed in September 2015) kept the strong job-growth over that year from boosting the pace of nominal wage-growth significantly. In September 2015, nominal wage growth over the past 12 months was 2.52 percent. In September 2016, it was 2.59 percent. Nominal wages do look to be on a very mild upswing, but remain far below any level that could be classified as healthy, let alone signalling an economy about to overheat.

After the September meeting of the Federal Open Market Committee (FOMC), Fed Chair Yellen indicated that the economy may still have “room to run”— meaning room to continue soaking up resources idled by insufficient demand in the economy. This strikes me as correct. The continued weakness in both wage-growth and interest rates are strong signals in this regard.

And gambling that the economy still has “room to run” carries much less-scary downside risks than gambling that we need to start containing inflation before it has appeared in the data. If the Fed tightens too late, the consequence is a short period of above-trend inflation that is (a) probably desirable and (b) amenable to predictable containment with steady interest rate increases. If the Fed tightens too early, the consequence is millions of workers without the full-time work they desire, and, tens of millions of workers that will see smaller inflation-adjusted wage increases than they otherwise could have had. Given that the stagnation in inflation-adjusted hourly pay for the bottom two-thirds of the american wage distribution is one of the most damaging economic failures of recent decades, this is a scary risk indeed.

Enjoyed this post?

Sign up for EPI's newsletter so you never miss our research and insights on ways to make the economy work better for everyone.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}